In June 1974, Henry Kissinger flew to Riyadh and shook hands on the deal that built the modern dollar: oil priced in greenbacks, oil revenue recycled into US Treasuries, US security guarantees in exchange. In May 2026, without a press conference, the UAE’s central bank told the US Treasury it might start selling its oil for something else.

That handshake had two legs. Invoicing crude in dollars held for fifty-two years. Recycling petrodollar surpluses into US Treasuries has been quietly unwinding since 2014.

The UAE’s letter is the moment the first leg formally cracks.

Why “1974 in Reverse” Is the Right Frame, Not “OPEC Drama”

The headline writers want this to be Gulf factionalism: the wobbliest OPEC member doing what wobbly members do, spats with Riyadh, internal politics. That framing buries the signal.

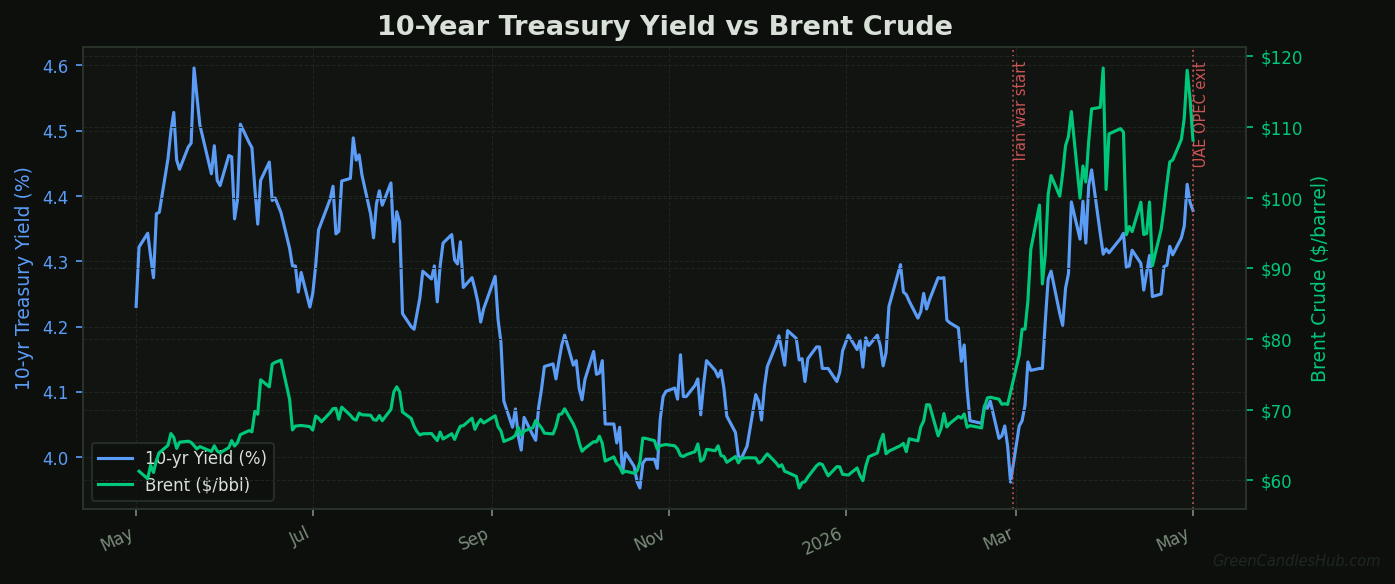

The UAE’s OPEC exit was reportedly paired with a parallel notification to the US Treasury about its intent to settle oil sales in non-USD currencies. If that holds, the bureaucratic letter, not the press release, is the part that matters. The OPEC exit can be reversed in a quarterly ministerial; a formal note to the Treasury cannot. Once a precedent exists, the cost of replication for other Gulf states drops to zero.

The under-reported piece is that the UAE has reportedly been doing this in practice since 2024. Rupee-denominated oil sales to India have been running for two years as live commercial flows, not as a pilot. The letter to the Treasury isn’t the start of Gulf de-dollarization — it is the formal acknowledgement of settlement that has been running on rupee, yuan, and gold rails since the Russia reserve freeze.

The Saudi Counter-Argument and Why It’s Late, Not Wrong

The smartest objection runs like this. Saudi Arabia hasn’t formally moved. OPEC+ remains USD-anchored. The vast majority of seaborne crude trade is still invoiced in dollars. UAE is the smallest mover, and gold’s rally is about real interest rates rather than monetary regime change.

This view is internally consistent and wrong on timeline rather than logic. Riyadh has been running yuan-oil pilots since the December 2022 MBS-Xi state visit, Aramco’s Chinese refinery joint ventures already accommodate non-USD settlement, and Iranian and Russian crude has been net-settling outside the dollar since 2023 — not in academic papers, in ship loadings. The “Saudis haven’t moved” framing confuses formal announcement with operational reality. They moved years ago and didn’t hold a press conference about it.

What the UAE letter changes is the bureaucratic friction. Once the Treasury has acknowledged a letter from a Gulf central bank stating non-USD oil settlement intent, the political cost for Riyadh to formalize what it is already doing collapses. The first formal mover absorbs the diplomatic incident; the followers come fast.

What Central Banks Have Been Saying With Their Balance Sheets Since 2014

The institutional vote on this question has been visible for over a decade. Central bank net gold purchases turned positive in 2014, the year of the Crimea sanctions on Russia, and never went back to neutral. Annual central bank gold accumulation accelerated roughly fivefold after the 2022 reserve freeze on Russia. That is a 12-year directional trend, not a cyclical trade.

Those flows happened across multiple Fed cycles, across positive and negative real yields, across QE and QT. The constant was institutional reallocation away from long-duration US Treasuries and toward a politically neutral monetary asset.

China’s UST holdings tell the same story from the other side. From the 2013 peak near $1.27 trillion, Chinese-held US Treasuries have been drawn down by roughly half — the largest sustained foreign holder rotation in modern Treasury history. The flow is steady, deliberate, and paired with physical gold accumulation that exceeds publicly disclosed holdings.

The Bank for International Settlements added the structural catalyst. Under Basel III’s revised liquidity framework, physical gold was reclassified as a tier-one asset on bank balance sheets — the same regulatory status as US Treasuries. UBS, Goldman Sachs, and JPMorgan flipped to structurally bullish on gold in 2024 and 2025. The institutional re-rating started before the UAE letter; the letter just made the headline line up with the flows.

The Trade: Long Gold Miners, Short Long-Duration USTs

There are three ways to express this thesis cleanly. The first is gold miners over physical gold. With spot above $4,000 per ounce, the major producers (Newmont, Barrick, the GDX basket) carry operational leverage that bullion cannot replicate. The marginal all-in cost of production at the largest miners runs around $1,400 to $1,600 per ounce. Every additional dollar in spot is roughly pure margin at scale.

The second is a structural underweight on long-duration US Treasuries. US debt-to-GDP just crossed 100% for the first time since World War II, the Iran war is layering spending onto the deficit each quarter, and the 10-year Treasury yield is already absorbing the structural pressure. Meanwhile the marginal foreign buyer is rotating away. TLT, the 20+ year Treasury ETF, is the cleanest public expression.

The third is the pair: long GDX, short TLT. Our gold-record outlook from late 2025 made the underlying case before the OPEC headline arrived; the UAE letter is the policy validation, not the trigger. The pair removes broad equity-market direction and isolates the spread.

The watch metric is bid-to-cover on US Treasury auctions. The post-2020 average on the 10-year ran around 2.5x. Sustained readings below 2.3x on consecutive 10-year and 30-year auctions through Q3 2026 is the moment foreign demand cracks; below 2.0x is the moment it breaks.

What Would Invalidate The Thesis

The first invalidation is Saudi Arabia formally re-affirming USD-only crude pricing while UAE walks back its Treasury notice within ninety days. That is the only clean path back to the 1974 architecture. On current evidence it looks unlikely, but it is the reversal to watch.

The second is a Fed pivot back to QE that re-establishes dollar liquidity dominance, collapses gold, supports long-duration USTs, and gives foreign buyers a reason to come back. The war-era short-term dollar bid is real, but a Fed pivot would slow the structural timeline, not reverse the destination.

The third is central bank gold flows reversing for two consecutive quarters without underlying USD reserve recovery — an actual re-rating, not a rebalance. The World Gold Council’s quarterly flow data is the canonical measure. None of the leading indicators suggest that’s coming.

The consensus that “until the Saudis move, this is just noise” will shift because the Saudis already moved. They just haven’t held a press conference about it.

The Saudi central bank’s H1 2026 reserve disclosure is the public confirmation many investors are waiting for, and the euro’s parallel reserve-asset moment is the same question coming from the European side. Neither confirmation is required: the balance sheets that matter have already moved.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Nothing here should be taken as a recommendation to buy or sell any security or asset. Always do your own research and consult a qualified financial adviser before making investment decisions.