Norway’s March trade surplus hit a three-year high — on $96 crude it didn’t cause and isn’t paying for. Britain, Italy, and France are being called the new “Piigs.” Both facts are products of the same war, and only one of them is getting coverage.

Every financial analysis of the Iran war has focused on costs: energy bills, sovereign debt stress, inflation revisions, central banks boxed into holding rates. That framing is correct as far as it goes. It just systematically ignores the other side of the ledger — the countries collecting the war premium rather than paying it.

The Trade Surplus Nobody Is Trading

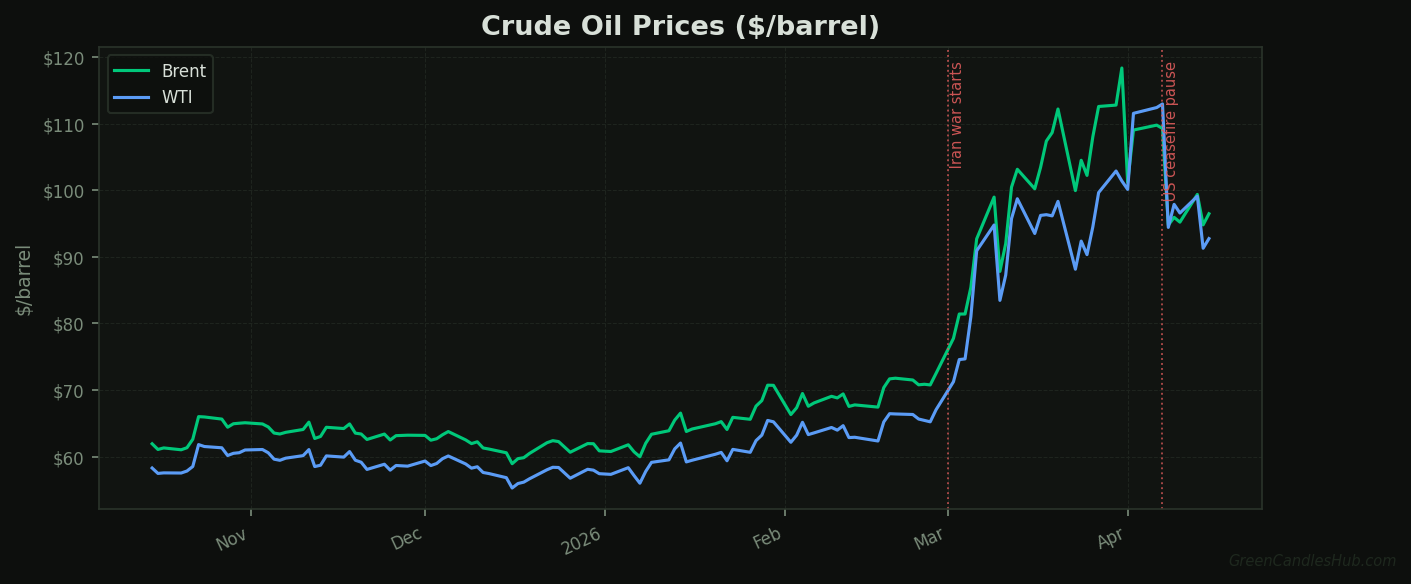

Norway’s crude exports surged to a record by value in March, driven by the oil price spike that followed the outbreak of war in the Middle East. Its trade surplus is now at the highest level in more than three years. The country produces approximately two million barrels per day from the North Sea. It is Europe’s largest oil and gas supplier. And it has zero operational exposure to the Strait of Hormuz.

None of this required any strategic decision on Norway’s part. North Sea production continues on its normal schedule. Equinor, the state-controlled oil major in which Norway holds a 67% stake, is pumping the same volumes it would have pumped regardless of events in the Gulf. The only thing that changed was the price. And the price changed dramatically.

Brent crude closed at $96.19 on April 15. That is roughly $30 above the price most analysts used in their 2026 fiscal models. For Norway, every dollar above the fiscal break-even price — estimated around $55 to $60 per barrel — flows into the Government Pension Fund Global. The windfall is structural and automatic. It requires no legislation, no emergency budget, no diplomatic effort.

What Equinor’s Balance Sheet Looks Like at $96 Brent

The Government Pension Fund Global is already the world’s largest sovereign wealth fund, managing approximately $1.7 trillion in assets as of late 2025. At current oil prices, its inflows are running well above the pace embedded in any previous long-term projection. Equinor (ticker: EQNR) captures the upstream margin directly, with North Sea costs per barrel that leave the current Brent price as pure rent at this level.

Compare this to the integrated oil majors with Middle East assets. Shell, TotalEnergies, and BP all face operational disruptions, insurance premiums for Gulf tanker exposure, and political pressure on their downstream positions in affected countries. Equinor has none of those complications. Its production is stable, its logistics are unaffected, and its revenues are maximized by the same supply shock that is disrupting its competitors.

The BIFs: Three NATO Allies on the Wrong Side of the Ledger

In the same week that Norway’s trade surplus data came in, the Financial Times named a new acronym for Europe’s sovereign debt problem: the BIFs. Britain, Italy, and France have borne the brunt of a sell-off in European government bonds sparked by the Iran war. The mechanism is structural: all three are significant net energy importers with high sovereign debt burdens and limited fiscal space to absorb the energy price shock through subsidies or budget expansion.

Italy depends on North African gas and Mediterranean-routed LNG; both supply lines have been disrupted. The UK has high retail energy price exposure and a gilt market that was already under watch before the conflict began. France runs nuclear-heavy electricity generation but has an exposed industrial base and a budget deficit the European Commission has been scrutinising for months. The IMF’s April 2026 World Economic Outlook issued a formal warning that the Iran war could tip the global economy toward recession — and the BIF sovereign spreads have been widening ahead of that call, not after it.

That detail matters. The BIF sell-off is not a reaction to a single news event. It is a structural repricing of countries whose fiscal trajectory has been negatively altered by the war premium in ways that compound over months. The spread widens not with headlines but with every energy import invoice and every revised growth forecast.

The Counter-Case: Norway’s Fiscal Rule Locks the Windfall Away

The standard objection is this: Norway’s fiscal rule limits annual government spending from the petroleum fund to 3% of the fund’s value. The windfall doesn’t flow into the Norwegian economy. It sits in the fund, deployed in global equities and bonds. So where is the NOK catalyst?

This argument is accurate as a description of Norwegian fiscal policy. It misses how sovereign credit markets actually reprice. Bond investors don’t wait for a government to spend its reserves before adjusting their view of its creditworthiness. They reprice on the direction of the balance sheet — and right now, Norway’s balance sheet is moving in one direction while the BIFs are moving in the opposite direction, for the same underlying reason.

Poland’s bond and currency repricing after Tusk’s election in December 2023 is the reference model. Markets moved on the shift in expected value — months before Brussels transferred a single euro. The direction changed; the market moved. The same logic applies here, except that Norway’s catalyst isn’t a political event that might be reversed. It is an oil price elevated by a conflict with no clear end date.

What the Divergence Trade Looks Like and What Closes It

There are three ways to express this divergence. The cleanest is sovereign spread: long Norwegian government bonds versus UK gilts or Italian BTPs. Norway’s fiscal trajectory is strengthening; the BIFs are under structural pressure. The trade doesn’t require a blow-up event to work — it just requires the current divergence to persist.

The equity expression is Equinor (EQNR). It benefits from elevated Brent directly, without the Middle East operational complications of integrated peers. At current prices, its free cash flow generation is running well above consensus models built before the war. The currency expression is NOK long versus EUR or a BIF basket — but NOK typically lags oil by three to six months, so this is the slowest of the three.

The trade has two caps. The first is a ceasefire. If Brent falls back toward $75 on a verified US-Iran agreement, the war premium dissipates and the divergence closes faster than sovereign spread dynamics alone would suggest. The structural US fiscal damage from the war doesn’t reverse on a ceasefire — but Norway’s surplus advantage narrows sharply if the oil price normalises. The nearest test: the two-week US-Iran ceasefire pause expires around April 21. If talks collapse and the blockade hardens, the war premium is repriced higher. If a deal is announced, Brent falls and the Norway windfall thesis compresses immediately.

The second cap is political. Norway’s NATO allies are paying for a war they collectively endorsed. Oslo has been notably quiet about the blockade’s legitimacy. Its sovereign wealth fund is growing at the fastest pace in years from a conflict that is economically straining its alliance partners. That dynamic has so far stayed out of formal diplomatic discussions. Whether it stays quiet through April 21 and beyond, as BIF sovereign spreads widen further, is a variable the spread trade cannot price — but cannot ignore.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Nothing here should be taken as a recommendation to buy or sell any security or asset. Always do your own research and consult a qualified financial adviser before making investment decisions.