$16.4 billion is too large to treat as background noise in the middle of an LNG chokepoint crisis.

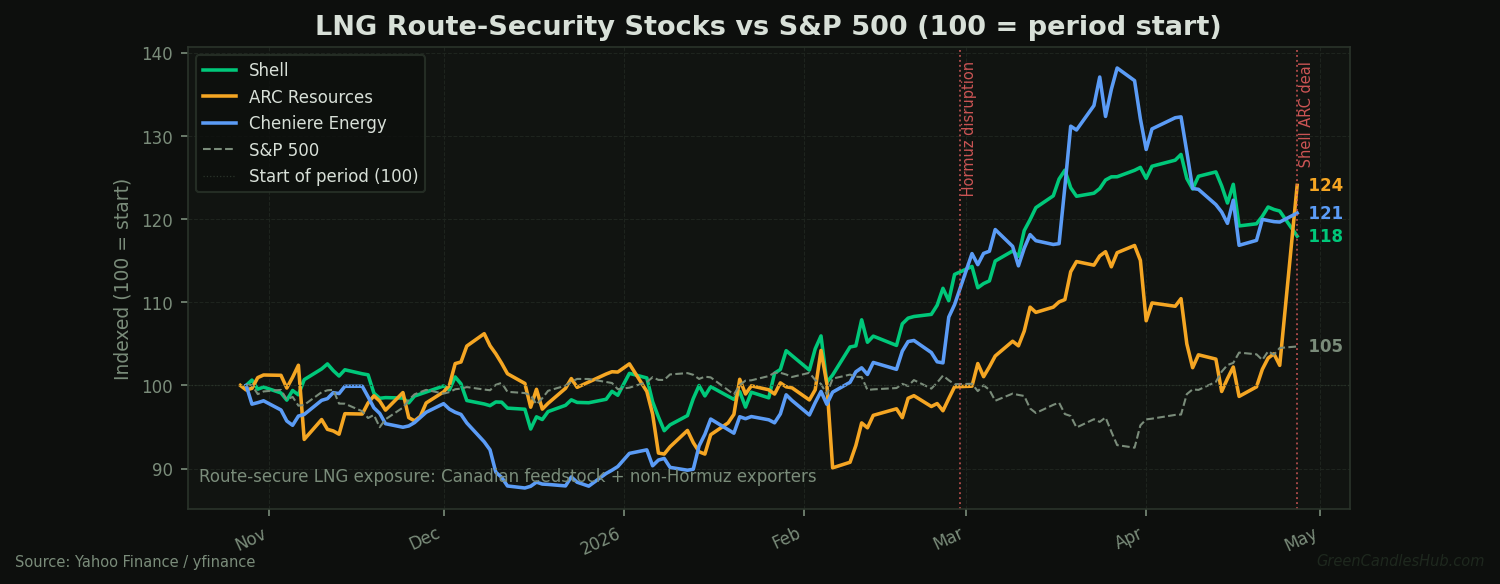

Shell agreed to buy Canada’s ARC Resources in a $16.4 billion deal, adding roughly 370,000 barrels of oil equivalent per day and access to about 2 billion barrels of reserves. LNG is no longer just a volume story. It is a route story. The headline version is simple: Shell wants more North American gas. The market version is sharper. Shell just bought more gas that does not need the Strait of Hormuz.

Qatar and the UAE sit inside the Gulf system. Canadian gas does not. When buyers are asking whether a cargo can physically move, the origin of the molecule starts to command a premium.

Why the Deal Looks Different After Hormuz

The lazy read is that this deal changes nothing. Shell has liked Canadian LNG for years. LNG Canada was already central to the company’s portfolio before the Iran war. ARC Resources was already one of the cleanest Montney gas producers available at scale. A buyer looking at Shell in isolation can call this basin consolidation and move on.

That misses what changed around the asset. Reuters reported that an ADNOC LNG tanker crossed Hormuz for the first time since the Iran war, and the fact that one vessel became a market event tells you how fragile the flow map has become. In a normal market, a tanker transit is plumbing. In this market, it is price discovery.

Shell did not need a war to justify Canadian gas. The war changed what Canadian gas is worth.

Canada Gives Shell Supply Without the Chokepoint

The acquired production sits in the Western Canadian gas system that feeds the LNG Canada corridor. Shell operates LNG Canada with a 40% stake, alongside Asian buyers that care less about branding than delivered reliability. The project’s location is the point: western Canada loads into the Pacific system rather than asking every cargo to survive Gulf politics, naval insurance, and delayed transit windows.

The market often values LNG projects as liquefaction capacity, but the scarcer asset in a stressed system is controlled upstream supply. A liquefaction train without dependable feedgas is an expensive booking option. A gas field tied to a Pacific export path gives Shell a stronger hand in term-contract talks, especially with buyers that want proof a cargo can arrive without relying on a Gulf reopening headline.

That makes ARC more than upstream acreage. It is feedstock control. For an LNG portfolio, feedstock control is what lets a company tell buyers that it has molecules, route access, and timing under one commercial roof. Geography decides whether an energy shock is a cost or a margin expansion. Norway’s crude export surge made the same point from the oil side.

The Qatar Replacement Trade Has a Capacity Ceiling

The bull case for U.S. LNG replacement supply has one weak joint: capacity is not the same as dependable full-year deliverability. Record exports can cover part of a shock for a while. They cannot erase maintenance schedules, feedgas constraints, weather disruption, or hurricane-season risk. If buyers lose Qatari or UAE cargoes for longer than expected, the marginal replacement cargo gets more expensive and less certain.

Hellenic Shipping News reported that only about seven ships crossed Hormuz in a 24-hour window as talks stalled. Normal commercial traffic through Hormuz runs in the dozens of vessels per day across tankers, LNG carriers, container ships, and dry bulk. Seven is not normal clearance. It is a warning that even partial reopening can leave buyers bidding for optionality before volumes normalize.

This is where Shell’s deal becomes more interesting than the headline multiple. If LNG cargoes from the Gulf remain uncertain while U.S. exporters run near their practical ceiling, a Canadian supply chain looks less like a long-term project and more like current insurance.

The Bear Case: Shell Paid for Volume, Not Optionality

The strongest objection is that management teams do not close $16.4 billion acquisitions because of a single conflict window. Shell has spent years shifting capital toward LNG because it sees gas as the transition fuel with the strongest long-duration demand profile. ARC fits that strategy even if Hormuz reopens tomorrow.

The pointed version is harsher. If Hormuz reopens before LNG Canada ramps fully, Shell may have paid a geopolitical premium for an asset priced as if that premium were permanent. In that version, the buyer gets good gas, but not the timing edge. The market then marks ARC as volume, not optionality.

The answer is yes — and investors don’t need Shell’s board minutes to reach it. The same 370,000 boe/d is worth more when Gulf LNG is unreliable than it was when Qatar looked like a frictionless global supplier.

That does not make Shell a clean long. It makes the acquisition a cleaner lens for how the market will value route-secure gas. If Brent and LNG risk premiums collapse below the war-premium range on a verified settlement, ARC goes back to being a scale story. If Hormuz remains a negotiated corridor rather than a normal shipping lane, Shell owns more of the supply chain buyers will pay to avoid disruption.

The insurance is not against gas scarcity alone. It is against route scarcity.

What Would Prove the Hedge Is Working

The first signal is Shell’s own language. Listen for management to talk less about generic production growth and more about LNG Canada feedstock, Pacific Basin buyers, and portfolio reliability. The second is contracting. If Asian utilities start paying up for Canadian or U.S. Gulf alternatives while Qatari timing stays uncertain, the market is validating the hedge.

The third signal is the clock. A sustained Brent range around the upper-$100s would tell investors the market still sees Gulf transit risk as unresolved, and the same uncertainty applies to LNG transit. The useful window is June and July, when maintenance and hurricane-season risk start to matter more for replacement supply. If Gulf cargoes normalize before then, the strategic premium fades. If they do not, Shell’s Canadian gas starts looking like insurance bought before the market knew how badly it needed it.

The question is whether Shell bought route security just as route security became the scarce commodity.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Nothing here should be taken as a recommendation to buy or sell any security or asset. Always do your own research and consult a qualified financial adviser before making investment decisions.