US annual interest payments crossed $1 trillion for the first time in history this year, according to Congressional Budget Office projections. That number arrived before the Iran war added military deployment costs, before the Supreme Court struck down a key tariff revenue assumption, and before the Federal Reserve signaled that rates would stay on hold for “some time.” Treasury Secretary Scott Bessent’s goal of bringing the US deficit to 3% of GDP was already demanding. It is now a number in a spreadsheet with no viable path to execution.

The question is not whether the fiscal math has changed. It has. The question is why Treasury markets have not repriced for it — and what forces the catch-up.

The Math That Was Always Optimistic

The US deficit currently runs around 6–7% of GDP. Getting to 3% requires eliminating roughly $1.4 trillion in annual deficit within the current term. Bessent’s strategy rested on three pillars: DOGE-style spending cuts generating hundreds of billions in savings, tariff revenue replacing some tax income, and nominal GDP growth expanding the tax base faster than spending grew. None of those three were delivering on schedule before February 28. DOGE claimed $150 billion in savings; independent estimates put realized cuts at under $30 billion through March. Tariff revenue faces legal challenge. Growth is being revised down.

The structural floor is the interest line. With $1 trillion in annual interest payments baked into the baseline, every month the Fed holds rates above 4% adds compounding cost. A single year of higher-for-longer translates to tens of billions in additional interest expense above the already-broken baseline. Bessent’s deficit target did not survive contact with that arithmetic even in peacetime.

Two Hits in One Week

Bloomberg’s read on Bessent’s position as of this week was direct: his goal has been undercut by the war and the tariff ruling arriving simultaneously. The Iran conflict is now in its fourth week. Members of the 82nd Airborne are deploying to the Middle East. A US naval armada is operating near the Strait of Hormuz. None of those costs appear in any current budget baseline. Emergency supplemental defense spending requests are not yet filed with Congress, but the operational tempo makes one inevitable if the conflict extends beyond 60 days.

The second hit is the Supreme Court ruling on tariff authority. Bessent’s projections assumed a specific tariff revenue trajectory. The ruling removed that assumption. Both events landed within the same week, compressing the already-narrow window to credible fiscal consolidation to zero.

The oil price compound makes the deficit math worse from both sides simultaneously. Brent crude near $100 inflates the nominal cost of government energy consumption and defence logistics. It also depresses real GDP growth — which is the denominator in the deficit-to-GDP ratio. Slower growth means more revenue shortfall and a wider ratio even before spending increases. The Economist’s analysis of the energy shock concludes that even a best-case ceasefire scenario leaves energy prices structurally elevated for months — which means the GDP drag and rate-hold dynamic persist well past any diplomatic resolution.

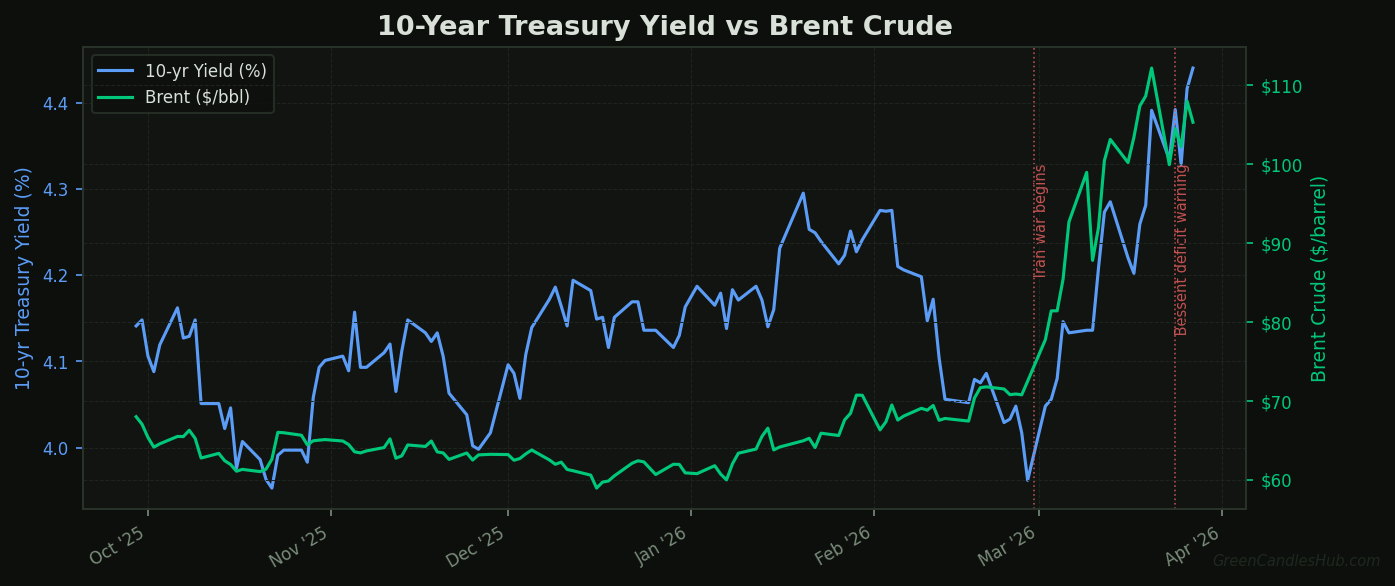

Why Bond Markets Are Lagging

The 10-year Treasury yield climbed from roughly 3.96% before the conflict to 4.26% in the first week of fighting. That is a real move. It is not a large enough move relative to the fiscal deterioration that has occurred since. The bond market appears to be pricing a short war — specifically, the scenario in which a ceasefire lands within weeks and the emergency defense spending request never gets filed. Oil slid below $100 this week when the US sent a 15-point peace proposal to Tehran via Pakistan. Stocks reversed losses when Trump cited progress in Iran talks. The market is priced for a negotiated exit, not a structural fiscal reset.

The dollar is absorbing part of the demand that would otherwise pressure yields. In past oil shocks, dollar safe-haven flows drove currency appreciation while simultaneously pressuring the Treasury market. This time, Barclays called the dollar rally a “bitter triumph”: the currency is rising, but White House policy uncertainty has capped the advance. The result is that safe-haven demand is split across the dollar and short-duration Treasuries — which means the long end is not getting the safe-haven bid that would anchor yields, and it is also not getting the fiscal-risk selloff that the deteriorating numbers warrant. It is priced for neither.

Barclays raised its S&P 500 forecast despite the war. Goldman Sachs reset its recession probability upward but not dramatically. No major house has made a high-conviction call that Treasury markets are pricing the wrong fiscal scenario.

What Triggers the Repricing

First: Congress receives a White House emergency supplemental defense spending request. This is the clearest catalyst. Every previous US military engagement of this scale has been accompanied by a supplemental appropriations bill. The moment that bill is filed, the deficit projection for fiscal year 2026 ratchets up in a single vote, and the 3% target gets its formal death certificate. The timeline is April–May 2026 if the conflict extends at current intensity.

Second: a Treasury auction shows weak demand. The bid-to-cover ratio on the 10-year is the earliest market signal. The April 10-year auction is the first one worth watching closely. A bid-to-cover below 2.3x on a consecutive basis — not a one-day anomaly — is the market telling you something real about appetite for long-duration US paper at current yields. According to Treasury auction data, that ratio has averaged around 2.5–2.6x over the past two years. A sustained step down is a different message than a single weak session.

Third: oil stays above $90 into Q3. Every quarter of elevated energy prices compounds two problems simultaneously: it keeps the Fed on hold, with Governor Michael Barr explicitly signaling rates may need to hold steady for “some time,” and it keeps real growth below trend, preventing the revenue recovery that would narrow the deficit. The longer oil holds above $90, the further the fiscal trajectory diverges from Bessent’s baseline.

What Traders Should Be Watching

The positioning implication is not short equities. Equity markets can reprice for higher rates without collapsing if earnings hold, and right now energy and defence earnings are expanding. The positioning implication is short long-duration Treasuries specifically, and the timing is tied to the two catalyst events above — not to oil levels alone.

TLT — the 20-plus-year Treasury ETF — is the clean expression of this view. Long-duration paper is the most exposed to a yield repricing driven by fiscal deterioration rather than growth expectations. If the market is currently pricing a short war and a resumption of the 3% deficit narrative, TLT is pricing the optimistic scenario. When that scenario becomes untenable, TLT falls faster than the 10-year because duration amplifies the move.

The internal risk is a genuine ceasefire. If Iran and the US reach a verified agreement and oil falls back toward $80, the Fed regains rate-cut optionality, growth reverts toward baseline, and the near-term pressure on Bessent’s numbers eases. That does not fix the structural $1 trillion interest floor — but it removes the immediate war-cost catalyst. A fast ceasefire compresses the timeline for the bond vigilante moment back to 2027 or later. The oil market’s own pricing structure makes a genuine fast resolution look less likely than the headlines suggest — but ceasefire risk is the trade’s primary stop-out condition.

For broader context on how this fiscal stress lands on EM sovereign positions — Turkey has already spent $30 billion defending the lira against foreign investor selling, and a Treasury repricing event would add pressure across the EM complex. The reserve drain dynamic is already in motion.

The two numbers to track: the bid-to-cover ratio at each 10-year Treasury auction through June 2026, and the date — if it arrives — when a White House supplemental defense spending request reaches Congress. The first is the market’s leading signal. The second is the fiscal event itself. Both are on the April–June calendar.

Disclosure and risk warning: This article is for informational and educational purposes only. It does not constitute financial, investment, or legal advice. All scenarios and trade ideas are presented for analytical purposes only. Investing involves high risk and you may lose capital. Always conduct your own independent research and consult a qualified professional before making any financial decisions.

Turkey’s $30 Billion Problem: How the Iran War Is Draining EM Reserve Buffers