The US dollar has risen roughly 2% since the Iran war began four weeks ago. In the 1991 Gulf War, it surged 8% over the same window. In the 1973 oil embargo it climbed even harder. Barclays has a phrase for what’s happening now: a “bitter triumph.” Oil is near $100. US troops are deploying to the Middle East. The classic ingredients for a flight-to-dollar are all present. The flight is not arriving.

The Safe-Haven Math Isn’t Adding Up

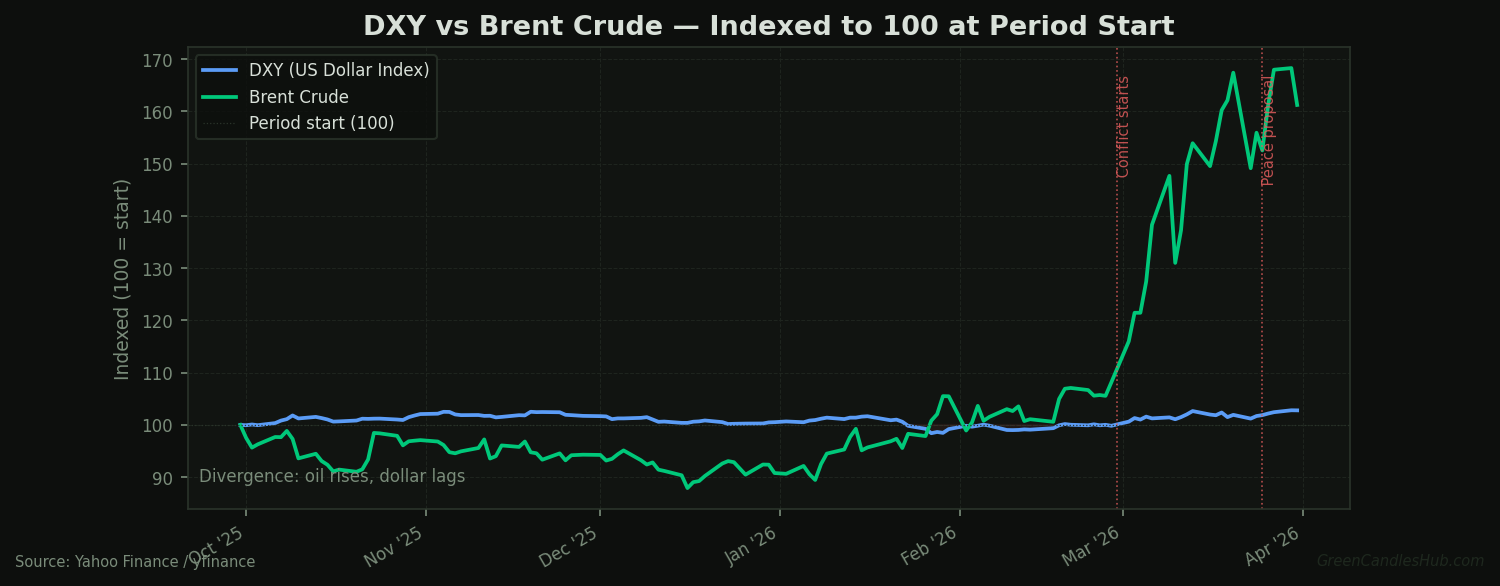

Petrodollar mechanics are straightforward: when oil spikes, dollar-denominated commodity settlement drives demand for USD. Capital flight from war-adjacent economies adds to it. In prior conflicts, both channels fired simultaneously. Today the first channel is running — Brent near $100 means dollar-denominated payment flows are elevated. The second channel is misfiring.

The Economist this week described markets as gripped by “an alarming cognitive dissonance” — investors all seem to believe everyone else is wrong. There is no consensus flight direction. Money is not concentrating in dollars. It is scattering: some into shorter-duration Treasuries, some into Swiss francs, some into energy equities, and some into nothing at all as margin calls force liquidations.

Two Forces Capping the Dollar

Barclays points to two specific headwinds. The first is White House policy unpredictability. The Trump administration sent a 15-point peace proposal to Tehran via Pakistan one day, then announced another wave of 82nd Airborne deployments the next. Markets pricing a USD safe-haven premium need a stable geopolitical narrative to hold that premium. They are not getting one. Every contradictory signal chips at the bid.

The second headwind is tech. In a normal risk-off environment, a weakening Nasdaq amplifies dollar demand as foreign holders of US equities repatriate. This cycle, US large-cap tech is itself under repricing pressure — AI capex stories are getting scrutinised, valuations are compressing — so the equity-to-dollar transmission is impaired. The dollar is not getting the multiplier effect it normally receives when both commodities and equity outflows push simultaneously in the same direction.

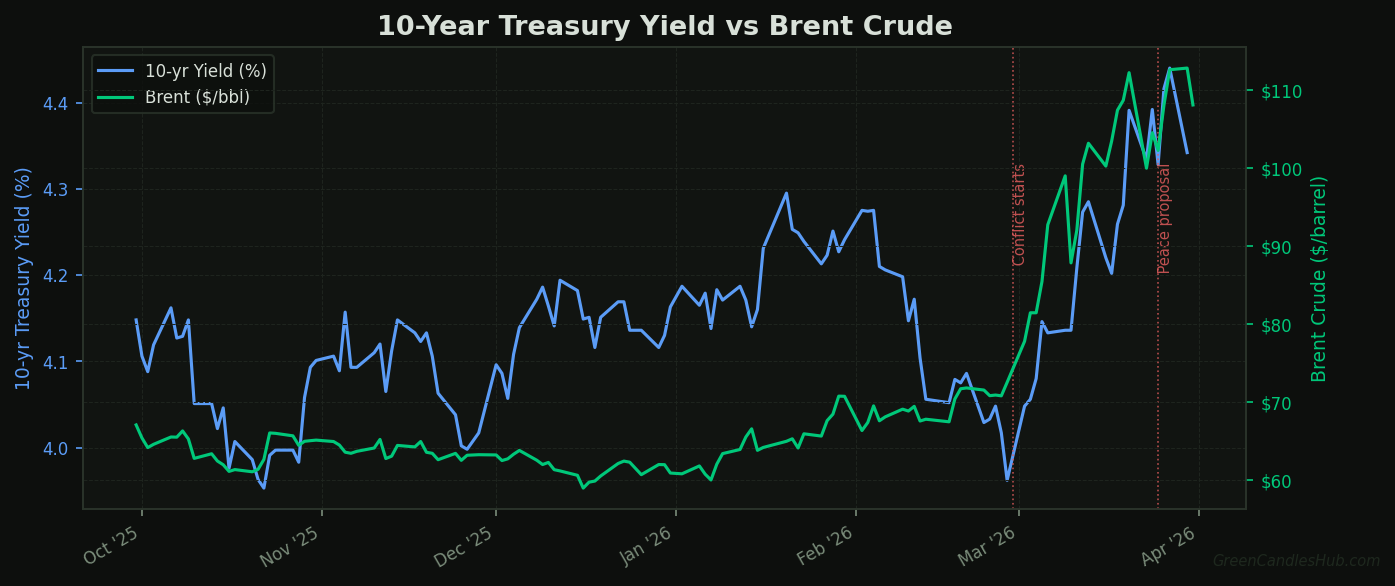

Then there is the Federal Reserve. Governor Michael Barr said this week that rates may need to hold steady “for some time” to address inflation still above the 2% target. No rate hike signal means no new carry-driven USD bid. In 1990, the Fed was actively tightening. The interest rate differential that normally amplifies wartime dollar strength simply does not exist at the same magnitude today.

Where the Money Is Actually Going

Gold’s haven status is under pressure. Margin calls are forcing liquidations in the precious metal — a pattern that has appeared in every major liquidity event since 2008. When portfolios need cash fast, gold gets sold regardless of the macro backdrop. The selloff does not mean gold is wrong as an inflation hedge. It means leveraged money is being unwound, and gold is one of the most liquid instruments available to raise cash quickly. The signal to watch is whether gold recovers its losses once the margin-call wave passes — historically it does, faster than any dollar rebound.

UK 30-year gilt yields pushed to 16-year highs, European bond spreads widened, and the Bank of England’s chief economist warned explicitly against letting “the fog of uncertainty” cause paralysis. Capital is staying regional. The European energy shock is driving inflation domestically, and European investors are not cycling into USD — they are hedging local duration risk. The dollar is losing the global capital aggregation role it played in prior crises.

For context on how this EM-dollar dynamic played out in Turkey and other war-adjacent economies, see our earlier analysis of Turkey’s reserve drain and the EM hidden risk from the Iran war.

The Hidden Risk: A Ceasefire Unwinds Everything

The asymmetry facing traders long dollars as an Iran hedge is brutal. If the war persists, the dollar grinds higher — but only modestly, because the cap forces described above don’t disappear. The upside is already largely priced. If talks succeed, the reversal is rapid and deep. The FT reported that Washington sent a 15-point peace proposal to Tehran via Pakistan. Oil slid below $100 on that single headline. Equities reversed losses within the same session.

A ceasefire simultaneously removes the war-premium from oil (dollar negative via petrodollar unwind), rallies risk assets (dollar negative via equity outflows reversal), and eliminates the flight-to-safety bid (dollar negative on all three channels at once). Traders who built USD longs as a war hedge face a scenario where all three exit pressures hit simultaneously. That is not the profile of a hedge. That is a crowded trade waiting for a catalyst.

Our earlier piece on what the Iran war means for oil traders argued that ceasefire headlines move prices while the physical market — the Dubai crude premium — tells the real story about duration. The same logic applies to the dollar: watch the DXY level, not the press conferences.

How to Position When the Safe Haven Is Broken

Avoid naked USD long hedges at current levels. The asymmetry is poor: capped upside if war persists, sharp downside on any credible peace signal. The Barclays “bitter triumph” framing is not just a colourful description — it is a risk-adjusted verdict.

Watch the DXY-Brent divergence as your primary indicator. When Brent stays above $95 but DXY fails to break its post-war high, the safe-haven breakdown is confirmed and accelerating. That spread has been widening since mid-March.

Gold on post-margin-call dips is the cleaner play once forced selling clears. The macro case for gold is intact: Fed paralysis, above-target inflation, no carry alternative, and a war that is not ending. Margin-call liquidations create entry points, not thesis changes.

Short-duration Treasuries over USD capture the Fed hold narrative — 2-year yields carry the rate-hold premium without the FX policy risk that comes from a White House that can reprice the dollar in either direction with a single Truth Social post. The carry is real; the currency risk is not worth taking as a hedge substitute.

The metric that matters in the next two weeks: if the US 15-point Iran proposal gets a formal response from Tehran, oil and risk assets will reprice before any ceasefire is official. Build your exit before that headline, not after.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Nothing here should be taken as a recommendation to buy or sell any security or asset. Always do your own research and consult a qualified financial adviser before making investment decisions.

Bessent’s 3% Deficit Target Is Dead. The Bond Market Hasn’t Priced It Yet.