The phones on rates desks started ringing before the New York equity open. A ceasefire headline crossed, oil slipped, and the first instinct was clean: buy duration, fade inflation, price cuts — in other words, bet that the worst is over and that easier monetary policy is coming. By the time traders parsed the latest Fed minutes, that tidy script looked far less durable.

My read is direct: this is not a one-tail macro shock anymore. It is a two-tail regime where the same geopolitical event can slow activity and keep inflation pressure alive through shipping and fuel channels. If you are priced for a straight glide into easier policy, you are holding the wrong shape of risk.

Why a Ceasefire Headline Does Not Clear the Inflation Channel

The consensus case deserves respect first. If conflict intensity drops, insurance premia should compress, tanker routes should normalize, and crude should lose part of its war premium. That chain usually feeds into softer gasoline and diesel prints within weeks. If that happens quickly, policy easing odds should rise.

The problem is the timeline. Shipping executives told CNBC that traffic through Hormuz may take “weeks, if not months” to normalize. That reflects physical mechanics, not diplomatic hedging. War-risk insurance riders have to be repriced by underwriters in London, convoy sequencing re-established with naval authorities, and charterers who rerouted around the Cape of Good Hope need contractual grounds to reverse mid-voyage. Each step runs on its own clock, and none responds to a headline.

That lag matters because energy pass-through is a flow problem, not a headline problem. Even if benchmark crude retraces, delayed physical movement can keep refined product pricing sticky long enough to distort one or two inflation prints. The market keeps trading the announcement. The Fed has to trade the realized lag.

What the Minutes Actually Said About Two-Sided Policy Risk

The minutes from the March meeting did not read like a committee preparing to declare victory. They read like a committee trying to preserve optionality. Officials discussed downside growth risk from the conflict while also acknowledging that higher fuel costs could push inflation back up and force a less comfortable policy path.

That is the detail most headlines blurred: two-sided risk is not neutral wording. It is an explicit warning against one-way market conviction. The policy range is still 5.25%-5.50%, and the communication posture says the committee wants room to react in either direction rather than validate a single easing narrative.

Why Europe’s Stagflation Signal Matters for U.S. Rate Pricing

The objection to using Europe as a parallel is obvious: the eurozone imports roughly 90% of its oil, the fiscal toolbox is more constrained, and the ECB runs a different mandate. Those differences are real. But the specific overlap that matters for the U.S. rate debate is narrower: whether an energy shock can produce simultaneous inflation pressure and growth drag within a developed economy that thought the worst was behind it. On that question, Europe is now producing live data.

A senior EU official warned in Bloomberg that stagflation risk still lingers despite the ceasefire. The warning came after a quarter of weakening eurozone PMIs alongside rising headline inflation driven by fuel and transport costs — exactly the two-tail pattern the Fed minutes described in a U.S. context. If Europe’s more energy-exposed economy cannot shake the overlap even with a truce in place, the assumption that a less exposed U.S. economy is cleanly immune to it deserves more scrutiny than it is getting.

The same week, the Financial Times reported OECD pressure on governments to rapidly unwind emergency fuel-duty cuts that more than 25 countries deployed during the war shock. Those cuts absorbed the consumer-facing price spike but masked the underlying inflation impulse. Removing them while supply chains are still normalizing risks a second-round pass-through — a pump-price jump that arrives not from a new shock but from the withdrawal of a fiscal buffer. For the Fed, even foreign fiscal decisions can feed back into U.S. inflation expectations through global fuel benchmarks.

The Positioning Error Is Pricing Relief Instead of Range

Most desks are not wrong to expect eventual normalization. They are early in treating it as complete. The pricing error is temporal: markets are discounting the destination while underpricing the messy path. In that setup, implied volatility at the front end can stay too low even if the end-state call is directionally right.

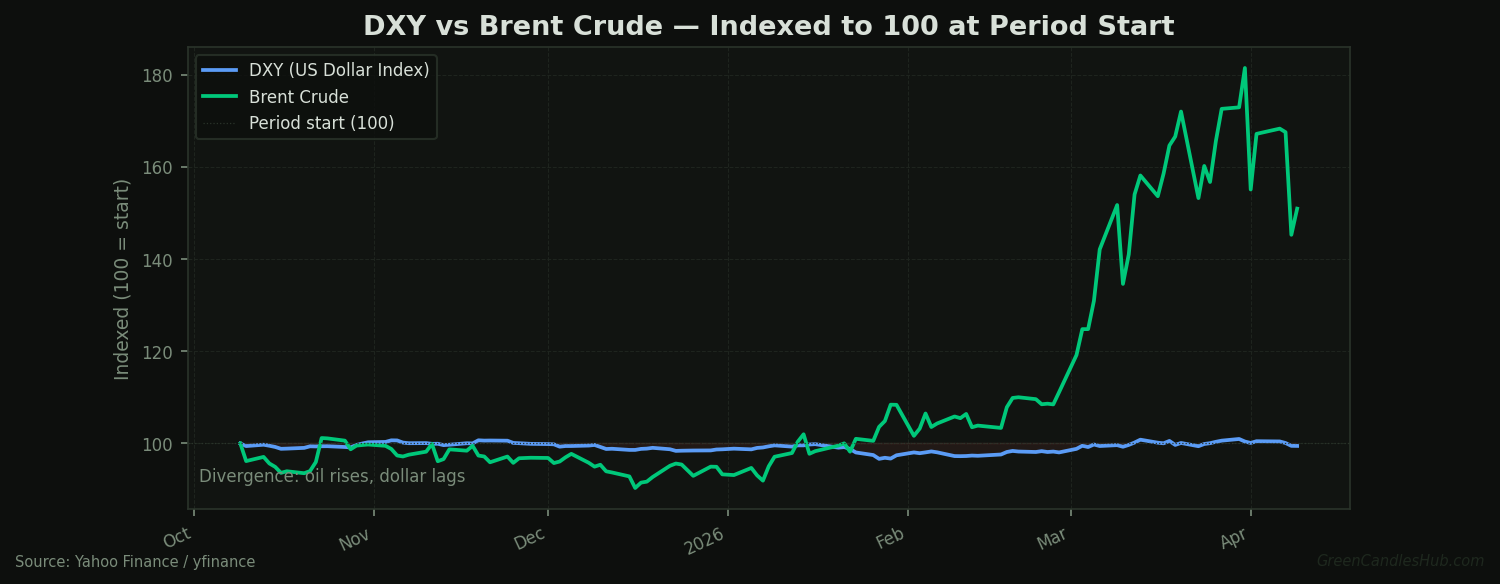

Translate that into scenarios. In scenario A, tanker throughput improves quickly and Brent drifts into the low $80s; then two-year yields can keep grinding lower and cut pricing extends. In scenario B, throughput stays constrained and Brent holds near the high $90s; then inflation compensation rebuilds while growth estimates soften, producing violent repricing in front-end rates. Current positioning still looks overweight scenario A.

The U.S.-specific asymmetry makes that tilt riskier than the headline numbers suggest. The EIA notes the Middle East Gulf supplied about 490,000 barrels per day, roughly 8% of U.S. crude imports in 2025. At the national level, 8% sounds absorbable. But those barrels are overwhelmingly medium sour grades feeding Gulf Coast and West Coast refineries that are tooled for exactly that crude slate. Replacing them requires sourcing heavier grades from Canada or Latin America, which carry different logistics costs and processing yields. The mismatch means regional refined-product pricing — Gulf Coast diesel, West Coast jet fuel — can move independently of headline crude, and those components feed directly into CPI transport and energy sub-indices.

That refinery-level friction is the same mechanism that drove the gasoline pass-through risk we mapped earlier this year, when a quieter macro week still produced a measurable inflation surprise through product-level pricing lags. The Iran disruption widens the variance around that channel by adding both a supply constraint and an insurance cost layer that did not exist in the earlier episode.

The One Screen to Watch Before the Next FOMC Window

If you want a practical signal, watch the joint behavior of Brent and the U.S. 2-year yield rather than either series alone. If Brent stays in a $90-$100 zone while front-end yields stop falling on soft-growth headlines, the market is telling you the inflation tail is still alive. In that case, terminal-rate pricing likely has to re-widen before it can trend lower again.

The expiry condition is clear. If tanker flow normalizes faster than expected, Brent breaks lower in a sustained way, and core inflation cools in the next release cycle, this disagreement thesis fails and a cleaner easing path can take over. Until that evidence arrives, the safer position is to treat the Fed as constrained by two tails, not liberated by one ceasefire headline.

Time-sensitive window: the view should be re-tested at the next CPI print and the following FOMC communication cycle. If those two checkpoints show softer core inflation with a stable energy complex, downgrade the two-tail thesis. If they show sticky services inflation with renewed fuel pressure, expect another round of policy-path repricing.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Nothing here should be taken as a recommendation to buy or sell any security or asset. Always do your own research and consult a qualified financial adviser before making investment decisions.