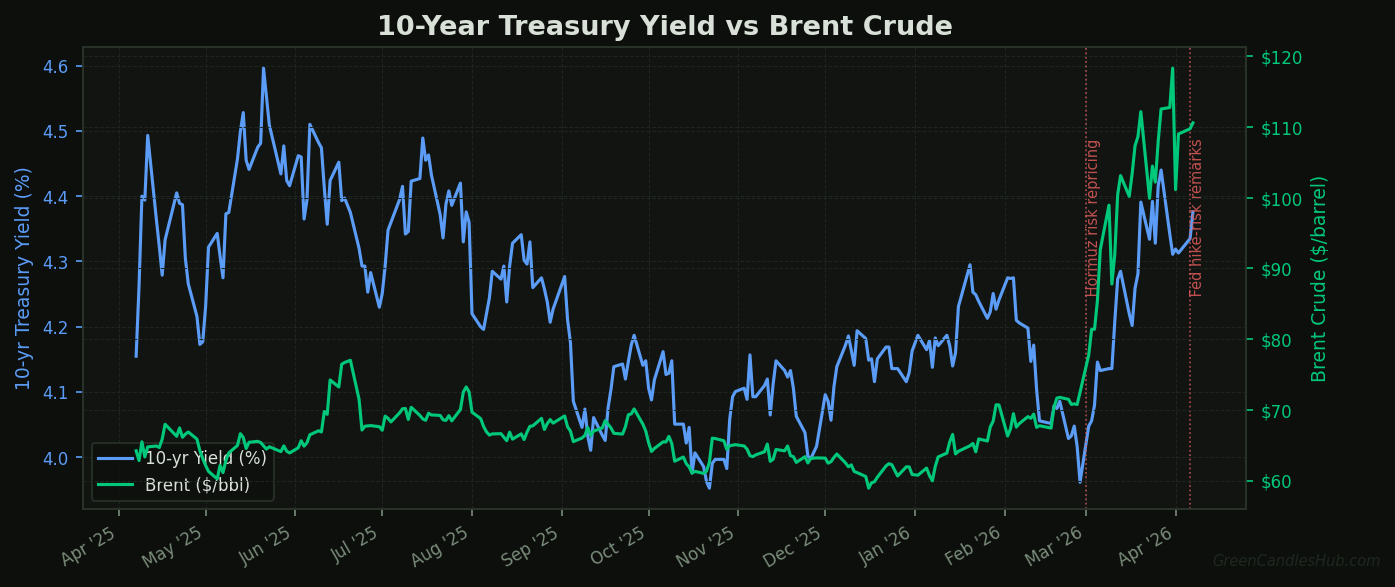

Most macro desks still treat this as an oil headline cycle that the Fed can ignore. Q1 2026 data already argues otherwise. The wrong frame is Brent alone. The policy channel is how quickly retail gasoline feeds into inflation expectations, then into front-end rates.

The consensus view deserves to be stated fairly: energy shocks are usually volatile, central banks look through them, and softer demand should cool core inflation later in the year. If that sequence holds, no hike risk is needed. But this cycle already shows a different mix of signals. A key Fed official has openly discussed possible hike risk tied to higher gas prices, while market pricing still leans toward a long hold.

Why Gasoline, Not Crude, Reaches the Fed Faster

Crude reacts in minutes to military and shipping headlines. Inflation policy reacts to what households pay at the pump and what firms pay in delivered fuel costs. That lagged retail pass-through is where monetary policy gets trapped: by the time the shock appears clearly in official inflation data, financial conditions have already shifted.

The hard data already points that way. The EIA reported sharp increases in crude and petroleum product prices in Q1 2026, which means the pipeline into gasoline and diesel was live before the latest policy commentary. Bloomberg’s inflation coverage also flagged that current US price behavior is showing uncomfortable similarities to the 2022 pattern of persistence, not a one-week spike.

For trading purposes, this means watching inflation transmission, not just commodity screens. We already broke down the first-stage energy move in our prior CPI-war snapshot. The new development is the policy language catching up to what product pricing has already done.

The Consensus Is Coherent but Still Misses the Second-Round Loop

The strongest counter-argument is simple: households cannot absorb another energy tax for long, so demand softens, and softer demand eventually drags inflation lower. That mechanism is real. It worked in prior episodes where energy moved first and growth rolled over quickly after.

The problem is timing. The Fed sets rates in real time against incoming inflation and expectations, not against the eventual slowdown six months out. If gasoline contributes a large share of near-term CPI upside, officials do not need a growth rebound to stay restrictive. They only need evidence that inflation progress has stalled.

This is where markets are likely underpricing risk. Many portfolios are positioned for “higher for longer” to remain a hold regime, not a hike-tail regime. A hike tail does not require base-case tightening. It only requires non-trivial probability that policy guidance shifts hawkish when the next inflation prints land.

Inflation expectations are the bridge between those worlds. A few hot gasoline weeks do not just affect household budgets; they can shift survey and market-based expectations enough to change how officials talk about risk asymmetry. Once communication shifts from “wait and see” to “cannot rule out additional tightening,” markets usually move first in the 2-year complex and then in valuation-heavy equity sectors.

Supply-Chain Reheating Can Keep CPI Pressure Alive

A pure gasoline spike might fade on its own. A gasoline spike plus logistics pressure is different. Bloomberg reported US supply chains straining in a way that resembles 2022, with diesel and transport stress reappearing in the data flow. That is the path from energy to broader goods and services pricing.

Once freight and distribution costs re-accelerate, the inflation impulse stops being an isolated pump story. It starts touching inventory policies, margin protection decisions, and delivery pricing across sectors. Companies that survived the first wave of post-pandemic cost shocks are less willing to absorb the second one in margins. They pass through faster.

The under-reported detail is that this loop can run even while growth narratives soften. You can have weaker sentiment and still have sticky near-term inflation prints. That combination is exactly what keeps front-end yields elevated and undermines early-cut positioning.

Another overlooked point is sequencing: if supply-chain pressure appears in producer prices before it appears in core consumer prints, traders get a narrow window to adjust duration and inflation hedges. Waiting for the full CPI decomposition can be too late, because the communication shift from policymakers often starts with the risk language, not the final table breakdown.

What Actually Confirms or Invalidates the Hike-Tail Thesis

Shelf life: time-sensitive. This argument expires quickly once the next CPI and Fed communication window passes.

Confirmation signal one: gasoline is a dominant contributor to the next headline CPI upside. Confirmation signal two: the 2-year yield stays firm or rises on that print instead of retracing. Confirmation signal three: Fed speakers continue to frame inflation risks asymmetrically, as seen in recent Federal Reserve communication.

Invalidation is equally clear. If gasoline contribution fades quickly, supply-chain stress indicators cool, and the 2-year backs down despite hot headlines, the market was right to treat this as noise. In that case, this reverts to a hold regime with no credible hike tail.

Until that invalidation appears, the cleaner trade expression is still rates-sensitive: watch front-end duration, inflation-sensitive equity multiples, and break-even behavior. The market does not need a full hiking cycle to reprice. It only needs to stop assuming that one is impossible.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Nothing here should be taken as a recommendation to buy or sell any security or asset. Always do your own research and consult a qualified financial adviser before making investment decisions.

The Dollar’s Hollow Rally: Why the Iran War Safe-Haven Trade Is Breaking Down