Oracle’s Dubai data center took an IRGC drone strike on April 2. The day before, Amazon’s cloud region in Bahrain was hit. The Islamic Revolutionary Guard Corps has now published a list of 18 US corporations with Gulf operations that it considers legitimate wartime targets — and not one of their stocks has adjusted to reflect what is an active, ongoing, named targeting campaign in its second month.

Two Data Centers in Two Days: What the IRGC Actually Hit

Oracle’s facility is its Cloud UAE East region, identified internally as me-dubai-1 (region key: DXB). Oracle also runs a second UAE cloud region in Abu Dhabi. Amazon’s Bahrain region — AWS me-south-1 — is the primary cloud infrastructure hub for the Gulf, supporting Saudi Aramco and multiple Gulf government clients. Both facilities were struck by IRGC drones within 24 hours of each other.

Oracle’s public status page showed no operational issues after the strike. That is a risk signal, not a reassurance. The IRGC’s drone attacks in this conflict have been probing in nature: mapping vulnerabilities and demonstrating reach before escalating to destructive strikes. Oracle’s clean status page confirms that the company’s disclosure framework is not calibrated for wartime infrastructure targeting. That gap between the physical event and the disclosed status will close, and probably in an earnings call.

The IRGC’s Sepah News stated after the Oracle strike: “For every assassination, an American company will be destroyed.”

It is a systematic escalation doctrine — consistent across two consecutive days of infrastructure strikes and multiple prior incidents — with a published corporate target list attached.

The 18-Company Hit List: Cisco, Oracle, JPMorgan, Tesla

Sepah News published the full list of companies designated as legitimate wartime targets: Cisco, HP, Intel, Oracle, IBM, Dell, Palantir, JPMorgan, Tesla, GE, Spire Solutions, Boeing, and UAE-based AI firm G42. The range matters. This is not a tech company list — it is cloud infrastructure, financial services, defence contractors, and industrial manufacturers with physical Gulf presences, all named in a single targeting document by an active belligerent.

JPMorgan operates corporate banking and wealth management across UAE and Saudi Arabia. Boeing has active defence export contracts with every major Gulf state. Palantir holds live CENTCOM and DoD contracts for war analytics — being named by the IRGC in a conflict where it is actively supporting US military targeting is not a marginal reputational issue. And Tesla, whose manufacturing exposure is not Gulf-based, now carries a novel category of geopolitical risk that its existing beta measures do not capture.

For context on how the IRGC has been escalating its financial leverage alongside these infrastructure strikes, see our analysis of how the IRGC is monetising Hormuz passage through stablecoins and yuan settlement.

Why Corporate Cloud Attacks Price Differently Than Military Strikes

Military asset strikes are absorbed into defence sector pricing and commodity markets within hours. Corporate infrastructure attacks run on a different clock. An Oracle or Amazon cloud region outage triggers SLA penalties, enterprise customer churn, insurance claims, and regulatory inquiries that surface in the next quarterly report — not the same afternoon. The market processes military risk in real time and operational corporate risk on a four-to-twelve-week lag.

Commercial data centres are not built to military-grade blast standards. A strike that fails to cause an immediate outage can still degrade cooling systems, damage fibre entry points, or compromise physical access controls in ways that only become visible under peak load. The IRGC’s pattern of probing before escalating is documented in every prior phase of this conflict.

AWS me-south-1 in Bahrain is not a redundant region for most of its customers — it is the primary region. AWS offers me-central-1 in UAE as an alternative, but many Gulf government and sovereign wealth fund workloads are contractually locked to Bahrain for data residency compliance. A sustained degradation scenario has no clean failover. AWS’s Service Health Dashboard is the first public signal of any confirmed regional outage.

What Options Skew on ORCL and PLTR Is Missing

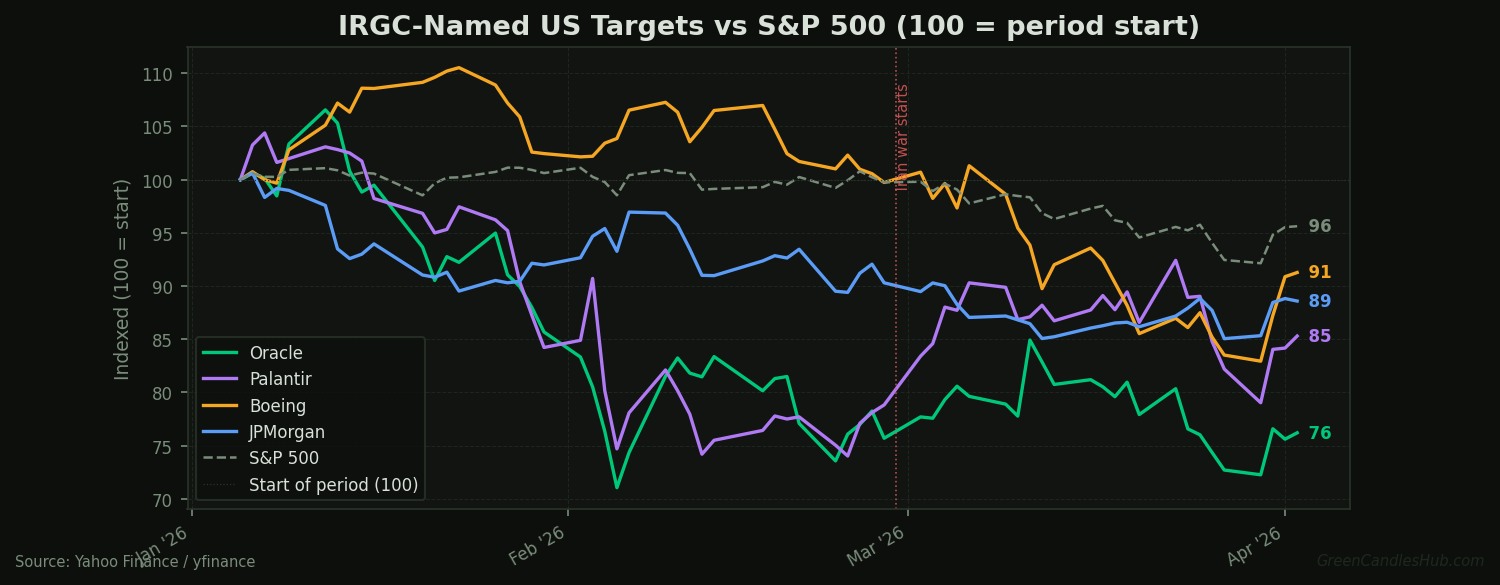

The mispricing is in the options market. Thirty-day implied volatility on Oracle (ORCL), Palantir (PLTR), Boeing (BA), and JPMorgan (JPM) has not moved relative to broader war-risk indices. The chart below shows all four named targets tracking the S&P 500 since early 2026 — the market is treating IRGC targeting designation as a news event rather than an ongoing operational risk with a published timeline.

Trump has stated the US will strike Iran “extremely hard” for the next two to three weeks. That puts the current intensification window through approximately April 20. During that window, the IRGC’s strike cadence — roughly one infrastructure target per day — is likely to continue or accelerate. Buying downside protection or volatility on named targets while this cadence holds is pricing disclosed risk, not making a speculative bet.

Palantir is the most asymmetric case on the list. It holds live contracts supporting US military targeting in this specific conflict, which makes its IRGC designation qualitatively different from a data centre operator caught in a regional sweep. The market has not separated these risk profiles. Palantir’s options surface shows no targeting premium at any tenor.

Watch Oracle’s Status Page and 30-Day IV Through April 20

The signal set is narrow and specific. Check Oracle’s cloud status page (status.oracle.com) and the AWS Service Health Dashboard daily for any undisclosed degradation in me-dubai-1 or me-south-1. A confirmed outage in either region — particularly one serving Gulf sovereign clients — would reprice the entire named-target cohort simultaneously. The correlation risk is high: all 18 named companies share the same physical threat geography.

On the options side, watch 30-day IV for ORCL, PLTR, BA, and JPM. The analytical watch threshold is 35%: if IV on any named target holds below that level while the IRGC strike cadence remains at one infrastructure hit per day, the market is still mispricing a publicly disclosed, active campaign. That gap closes either in the stock price or in the volatility surface. Trump’s stated intensification window ends around April 20 — that is the deadline for the risk-discounted entry. After that date, the calculus shifts depending on whether a ceasefire framework has emerged.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Nothing here should be taken as a recommendation to buy or sell any security or asset. Always do your own research and consult a qualified financial adviser before making investment decisions.