I’ve been staring at Hungarian government bond spreads since Sunday night and I still can’t tell whether the \u20ac20 billion question is already priced or whether the market hasn’t connected the political result to the fund flow math.

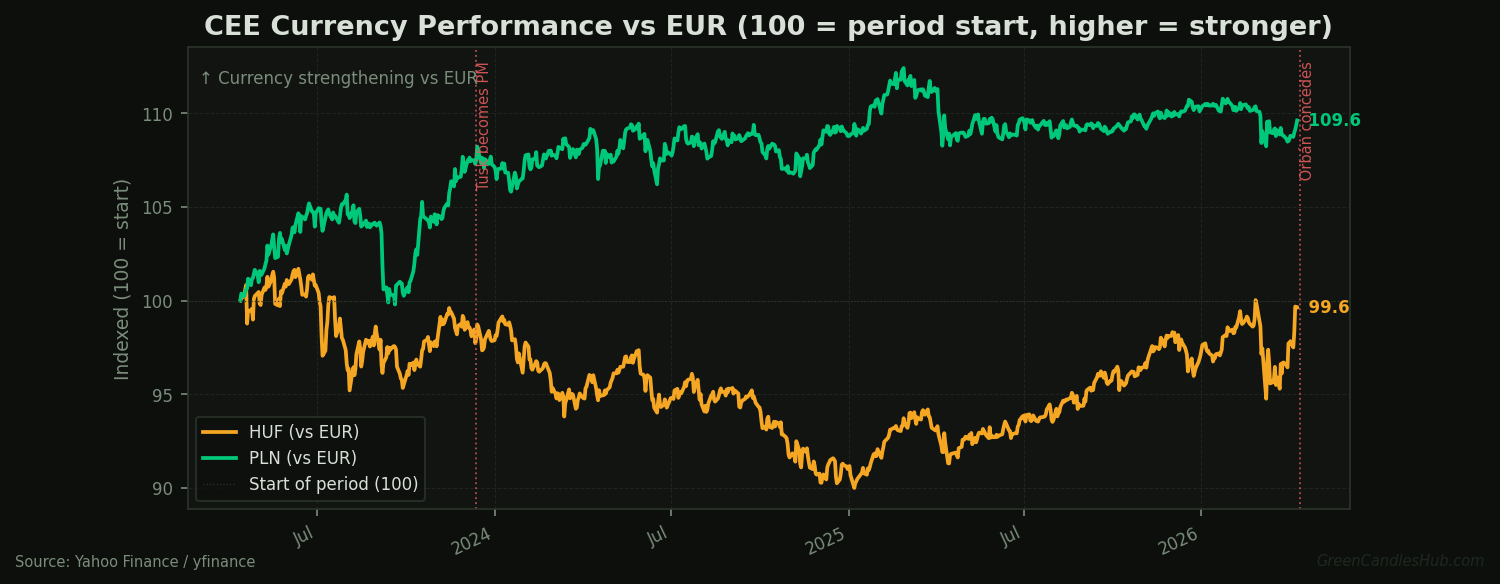

The Financial Times projected Tisza winning a two-thirds majority in Sunday’s Hungarian election, with Orbán conceding defeat. The headline is the end of Fidesz’s sixteen-year grip on Hungary. The market question is what two-thirds specifically unlocks, and on what timeline.

Why Two-Thirds Is Not the Same As Just Winning

A simple parliamentary majority lets you govern. A constitutional supermajority lets you restructure the institutions the EU has been demanding Hungary restructure for five years. That distinction matters because the EU’s frozen fund conditions were not generic democratic concerns — they were tied to specific constitutional court appointments and anti-corruption oversight mechanisms that require a two-thirds mandate to change.

The EU’s Article 7 rule-of-law proceedings and the Recovery and Resilience Facility conditionality both named judicial independence as the blocker. The European Commission’s Hungary RRF assessment listed independent court supervision and anti-corruption agency powers as the primary unresolved milestones. Tisza can move on those immediately, without coalition negotiation. That removes the procedural ambiguity that dragged Poland’s fund release for months after Tusk’s narrower December 2023 mandate.

The \u20ac20 Billion Breakdown: What Flows and When

Hungary has roughly \u20ac10.2 billion frozen in the Recovery and Resilience Facility, with pre-agreed milestones already documented by the Commission during 2023–2024 negotiations. A further \u20ac7 billion in cohesion and structural funds sits frozen under separate rule-of-law conditionality. Combined, that figure exceeds 10% of Hungary’s annual GDP (figures per the European Commission’s Hungary RRF assessment) — an exceptional fiscal injection by any EU standard.

The timeline that matters is not when Budapest spends the money. It is when the market prices the probability of it. Brussels had the release framework ready before Sunday; what was missing was political compliance on the Hungarian side. That compliance arrived with a constitutional supermajority.

Poland is the reference point. The zloty began repricing within weeks of Tusk’s election in December 2023 — months before the EU transferred a single euro. The Polish recovery trade played out on trajectory, not on disbursement confirmation. The market moved on the change in expected value, not on the realised cash flow.

The Counterargument: Brussels Moves Slowly, and Tisza Has Orbán’s Mess to Clean Up

The bearish case is not stupid. EU disbursement has historically lagged political change by twelve to twenty-four months. Conditionality milestones are complex and subject to Commission interpretation. Tisza inherits an economy built around Fidesz’s fiscal preferences — state subsidies, structural deficits, inflation running at roughly 5% annually as of early 2026, above EU averages. The government they ran against is the government whose accounts they are now opening.

None of that negates the catalyst. Asset repricing is about expected value, not certainty. The probability that \u20ac20 billion flows toward Hungarian public finances shifted substantially on Sunday. That shift happens in days. Disbursement happens in quarters. Waiting for the first payment confirmation before buying is not front-running anything.

What the Bond and FX Markets Haven’t Done Yet

Hungarian government bonds trade at a meaningful spread premium to German bunds — a premium that widened specifically because of the rule-of-law conflict, not because of Hungary’s underlying creditworthiness versus CEE peers. The HUF carry trade has been structurally underweighted because of Orbán’s political risk premium — the premium that made institutional allocators treat Hungarian assets as a category of their own within CEE.

That category separation is now dissolving. Not instantly, but directionally.

The cleaner expression than a directional HUF call is the spread trade: long Hungarian government bonds versus the broader CEE sovereign index. The repricing thesis is Hungary-specific; the risk management is therefore also Hungary-specific. The catalysts — EU milestone certification, Commission disbursement decisions, Tisza’s first parliamentary acts — are all observable and dateable.

The Question Nobody Is Asking About Orbán’s Back Channel

For the past three years, Orbán was the one EU leader who maintained personal working contact with the Kremlin. Multiple European capitals used him as an informal relay for communications that couldn’t travel through official diplomatic channels. Whether anyone officially admits this matters less than the operational reality: that conduit disappears with the coming handover.

The explicit version of this leverage was Orbán’s veto threats on EU Russia sanctions packages — most visibly on the 14th package in 2024, where Budapest held out for weeks before voting yes after extracting Hungarian-specific energy carve-outs. The implicit version — the back-channel conversations that shaped what came to the table before formal votes — is harder to quantify but probably more consequential for EU-Russia energy negotiations going forward.

What this means for European sanctions coordination over the next twelve months remains unclear. The simple read is that EU decision-making gets faster and more coherent without a veto threat in every room. The complicated read is that losing the Moscow back channel removes information the EU was receiving informally — information that will now have to come through official channels, which are slower and less candid. I don’t have a confident position on which version dominates. What I can say is that the back-channel question has a direct bearing on the bond trade. If markets read Orbán’s exit as a clean break from Moscow risk — Hungary shedding its geopolitical ambiguity — that accelerates spread compression. If they read it as Hungary losing a structural buffer in a region still exposed to Russian energy, it complicates the risk-premium story. The two readings point in opposite directions on the HUF and the bond spread; which one the market lands on matters as much as the EU fund timeline.

Which Template Does Brussels Choose?

The two market framings in circulation are the Poland template — front-run the fund flow, buy HUF, compress the spread before Brussels moves — and the EU-bureaucracy template, which says wait for the Commission to certify milestones before repositioning.

What I can’t resolve is which one Brussels itself wants to validate. The Commission has a strong incentive to move fast on Hungary’s fund release ahead of the 2027 European Parliament elections. A successful Hungarian transition would be the clearest demonstration available that EU democratic-norms enforcement actually works. Commission President von der Leyen immediately hailed the result on election night, stating that “Hungary has chosen Europe” — a signal that Brussels intends to make this a fast, visible transition rather than a quiet bureaucratic one. If that framing holds, the timeline compresses and the Poland template applies.

If Brussels treats this the way it treats most rule-of-law processes — carefully, with extensive milestone certification and legal review — the timeline extends. The spread trade still works. The catalyst is just slower.

I don’t know which version we’re in yet. That’s the question.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Nothing here should be taken as a recommendation to buy or sell any security or asset. Always do your own research and consult a qualified financial adviser before making investment decisions.

Fed Hike Tail Risk Is Back via Gasoline