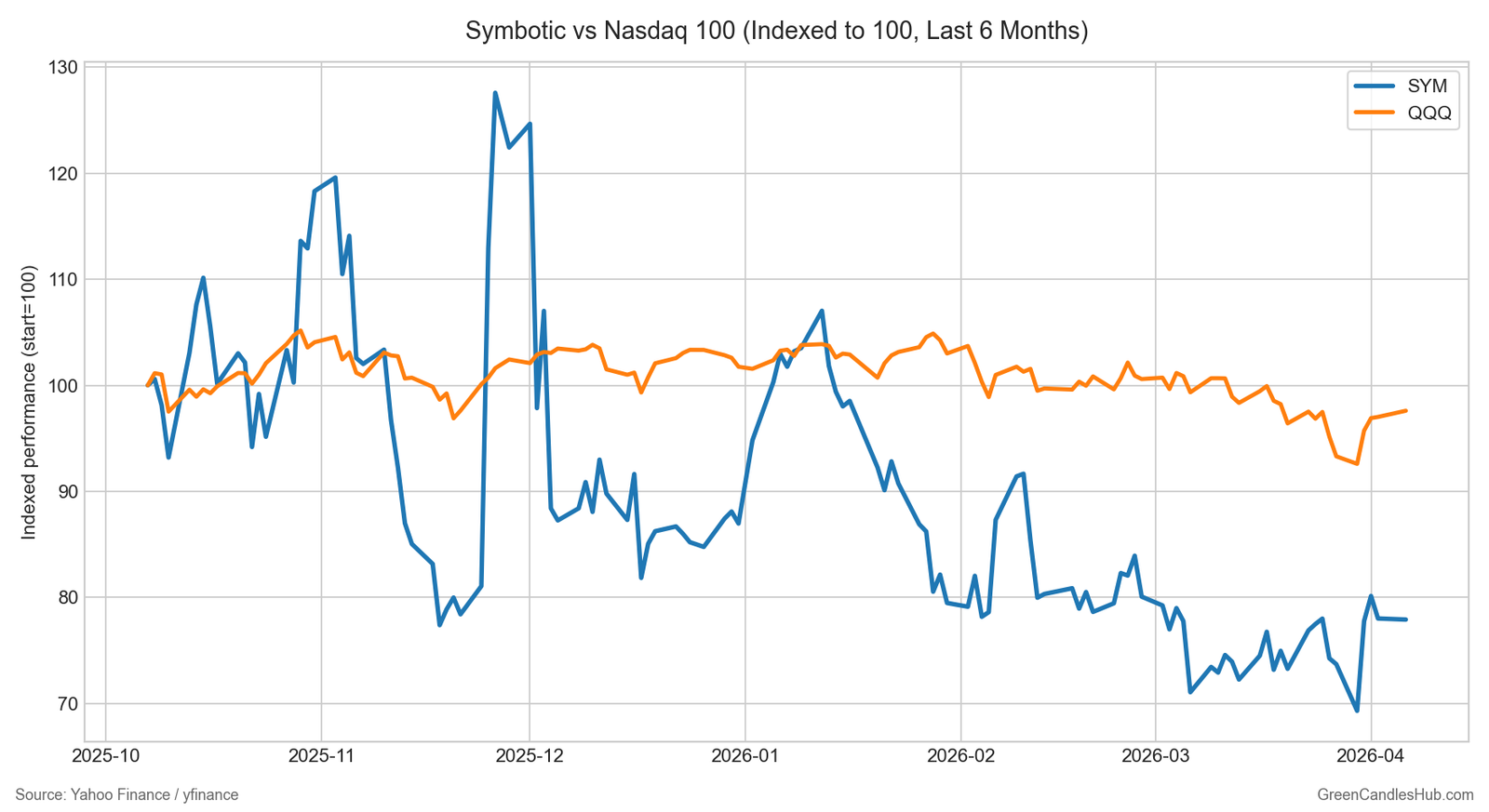

51,000 tech jobs were reported cut in 2026, yet Symbotic traded around $53.30 pre-market on April 7. That divergence is not noise. Capital is leaving broad labor-heavy tech while still funding automation names that can convert signed contracts into accepted systems. Symbotic is a clean read because its progress is physical and auditable: systems are either deployed and accepted, or they are not.

This is a trade note for one catalyst window: the next Symbotic quarterly print, expected in early May 2026.

The Symbotic Numbers That Actually Matter This Quarter

Start with what Symbotic reported in its latest quarter (Q1 FY2026 filing materials): $630 million revenue, $66.9 million adjusted EBITDA, and 21.2% GAAP gross margin (23.4% adjusted gross margin). Remaining performance obligations were $22.3 billion, and management expects about 13% to convert in the next 12 months, with 62% converting in months 13-60. That is a multi-year queue, but it is also a timing risk if deployment slips.

The trajectory across recent periods is constructive but tight. In Q3 FY2025, Symbotic did $592.1 million revenue and 18.2% gross margin; in Q4 FY2025, $618.5 million and 20.6%; in Q1 FY2026, $630 million and 21.2%. Adjusted EBITDA moved from $45.4 million (Q3 FY2025) to $49.4 million (Q4 FY2025) to $66.9 million (Q1 FY2026). This is clear operating leverage, but the setup is not diversified: one customer represented 85.6% of Q1 revenue, and Walmart plus Exol still drive most backlog.

That customer concentration is why this cannot be treated like a generic industrial momentum trade. Symbotic can print strong margins and still reprice hard if acceptance timing shifts at a single large customer node.

Deployment Throughput Is the Real Constraint, Not Demand Headlines

Warehouse automation is not a download. Revenue depends on site preparation, hardware integration, testing, acceptance milestones, and go-live reliability at customer facilities. That creates timing friction that many AI investors still underestimate. In other words, demand can be real while realized revenue still lags for two quarters.

Symbotic’s own contract language confirms this timing structure: most systems revenue is recognized during deployment milestones, then software maintenance and service streams rise after acceptance. The market will tolerate backlog volatility. It does not tolerate deployment slippage when valuation already reflects a smooth conversion path.

The 51,000-layoff backdrop matters here because it keeps pressure on management teams to prove hard ROI before expanding automation budgets. That supports high-conviction projects and delays marginal ones. Symbotic’s backlog is large enough to absorb some pacing noise, but quarter-to-quarter conversion still decides whether the stock trades as execution premium or concentration discount.

SF at $2.15M Confirms Capital Concentration, Not Broad Cycle Strength

Bloomberg reported San Francisco’s median home price at $2.15 million in March, up 18% year-on-year. That is a concrete sign of AI-linked liquidity hitting local assets. It also highlights a policy and valuation tension: wealth effects can be strong in a few ZIP codes while labor outcomes remain mixed across the broader tech workforce.

For SYM, this macro split explains valuation behavior better than generic \”AI demand\” talk. Asset prices in AI-heavy hubs are inflating, while broad hiring is still under pressure. In that environment, investors pay for delivered automation, not for promise. Symbotic gets paid if deployments convert on time and margins hold. It gets punished if either piece wobbles.

Peer context reinforces the point: AutoStore printed 73.7% gross margin in Q4 2025 on an asset-light model (company release), while Symbotic is around 21%. These are different models and should carry different multiples. The right SYM test is not whether it can look like software. The test is whether it can keep lifting margin from high teens into low twenties while scaling systems revenue over $600 million quarterly.

Single Trigger, Timeline, and Sizing Rule

Catalyst window: next earnings print (expected early May 2026), then confirmation in the following quarter.

Trigger condition that changes the position: move to an overweight only if the company prints both (1) GAAP gross margin of at least 21.0% and (2) remaining performance obligations still above $22.0 billion with 12-month conversion guidance at or above 13%. If either breaks (margin below 20.0% or RPO falls below $21.5 billion with weaker 12-month conversion language), cut exposure.

Position sizing implication: hold half-size into the print while the setup is still concentration-sensitive. Add to full size only after the release if both trigger conditions are met. Reduce to quarter-size or flat if one condition fails, because history in execution-led names shows that margin slippage and conversion slippage usually rerate together once they appear.

This keeps the trade tied to Symbotic-specific mechanics: a $22.3 billion RPO base, a 13% next-12-month conversion profile, a margin climb from 18.2% to 20.6% to 21.2%, and revenue concentration above 85% in one customer channel. If those numbers hold, the current premium is defensible. If they crack, it is not.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Nothing here should be taken as a recommendation to buy or sell any security or asset. Always do your own research and consult a qualified financial adviser before making investment decisions.