Trump Media & Technology Group is merging with TAE Technologies in a $6 billion all-stock deal that will create one of the world’s first publicly traded nuclear fusion companies. The merger was announced in December 2025. Each company ends up owning roughly 50% of the combined entity. TMTG committed $200 million in cash to TAE upon signing, with additional cash to follow. The deal requires shareholder approval and is expected to close mid-2026.

Most commentary has treated this as another Trump brand extension — a meme stock in a new costume. That framing is incomplete. Before December, DJT moved almost entirely on Trump’s political fortunes. After the merger closes, it will move on two independent variables: Trump’s approval ratings and energy crisis severity. Those two drivers are not correlated. That structural shift is the trade, and most investors covering the stock have not updated for it.

TAE’s Boron-Proton Approach Is the One Fusion Bet Without Tritium

The dominant fusion approaches — Commonwealth Fusion, Helion, ITER — all work with deuterium-tritium reactions. TAE Technologies does not. TAE pursues proton-boron fusion: a reaction between hydrogen-1 and boron-11 that produces three helium nuclei, no neutrons, and no radioactive waste. No tritium breeding required, no proliferation risk, no radioactive blanket management.

The tradeoff is plasma temperature. Deuterium-tritium ignites at roughly 100 million degrees Celsius. Proton-boron requires approximately 3 billion degrees. TAE’s Norman device reached 75 million degrees Celsius in 2022 — a genuine milestone that was widely covered. The gap to ignition was not.

That gap is the specification of the bet, not a disqualification. TAE has raised over $1.2 billion in private capital since its 1998 founding, per TAE Technologies’ company filings. Its backer list includes Google, Chevron, and Vulcan Inc. (Paul Allen’s estate). The Chevron investment, made in 2022, deserves specific attention: this is the same Chevron now negotiating a $7 billion natural gas plant in West Texas with Microsoft and Engine No. 1 to generate 2,500 MW of AI data center power. Chevron is hedging across fossil gas now and fusion later.

The Iran War Changed Fusion’s Political Calendar Without Changing Its Physics

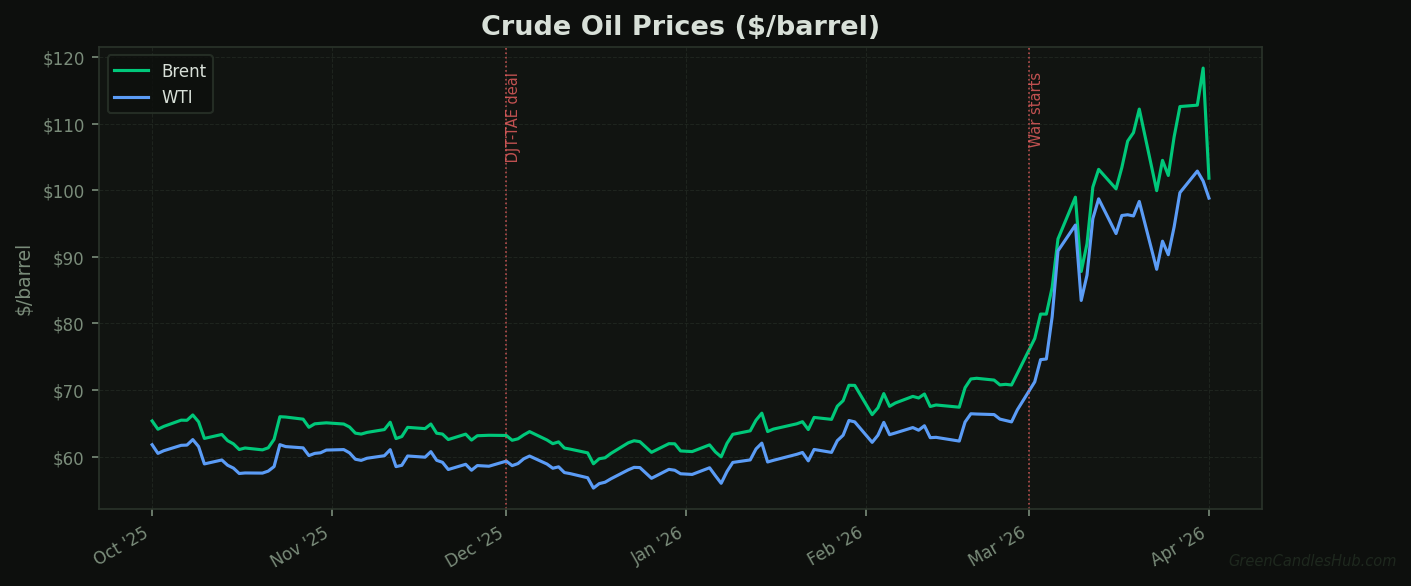

Before March 2026, fusion had broad bipartisan support in theory and weak funding urgency in practice. OPEC was producing above 28 million barrels a day. Spot LNG was trading near multi-year lows. The political conditions that typically accelerate advanced energy programs — the kind of urgency that moves procurement budgets rather than just policy papers — were absent.

The war changed that fast. OPEC produced just 21.57 million barrels a day in March, per Reuters’ March OPEC production survey — the lowest output since June 2020, when pandemic lockdowns had effectively stopped the global economy. Kuwait, Iraq, the UAE, and Saudi Arabia all cut production as the Strait of Hormuz conflict choked their export routes. Asian spot LNG prices surged 70% since the war began, with energy-intensive factory sectors contracting across the region while China’s domestic demand held on stimulus expectations.

For the full restructuring of crude markets since the conflict started, see our analysis of how the Iran war moved oil prices. The relevant point here is more specific: the energy security emergency has shifted fusion from a long-term research line item to a near-term procurement priority. TAE’s commercial demonstration target is 2027–2028. Whether it meets that date, government funding interest and private capital appetite for energy diversification bets are structurally higher than they were twelve months ago.

DJT was a single-factor stock. The TAE merger adds a second factor with a different sensitivity profile. That is what changes the position’s risk-reward geometry.

Three Risks Most DJT Investors Are Not Pricing

The political-sentiment framework most analysts use to model TMTG produces clean, single-variable models that miss all three of the risks this deal introduces.

Fusion timeline risk. TAE has not demonstrated net energy gain — no fusion company has in a proton-boron configuration. TAE’s commercial demonstration target has already slipped from earlier projections. A further delay past 2028 removes the energy urgency narrative while the combined entity burns through the $200 million TMTG cash commitment on experimental plasma physics. The stock would then need to be re-rated purely on Trump sentiment with a much weaker balance sheet.

Deal-close risk. The merger requires approval from TMTG’s retail shareholder base, which is politically motivated and may not be aligned with an energy technology pivot. DJT’s investors bought a media company. A contested shareholder vote, or an SEC request for supplemental disclosure, pushes the close past mid-2026 and compresses the merger premium. The Form S-4 registration filing date with the SEC is the earliest hard indicator of whether the timeline holds.

Media stub risk. Truth Social generated approximately $3.6 million in revenue in Q3 2025, per TMTG’s Q3 2025 10-Q filing. That is the non-fusion value floor. Brent fell below $100 per barrel this week on de-escalation signals from the White House. If the energy crisis eases faster than TAE’s commercial timeline advances, the combined entity loses both its political premium and its strategic narrative simultaneously. The stub is not a floor in that scenario.

Watch the S-4 Filing Date, Then Brent, Then TAE’s Plasma Progress

The Form S-4 registration statement filed with the SEC is the key timing signal. A filing before April 30 confirms no material adverse change clause has been triggered and puts a June shareholder vote within reach. If the S-4 slips to May or later, timeline risk rises and DJT typically re-rates toward its political-sentiment floor — historically 30–40% below its merger-premium price depending on where the stock is trading relative to the implied deal value.

Q1 2026 set a record for megadeal volume — 22 transactions above $10 billion in a single quarter — and deal close rates historically improve in high-M&A environments as regulatory reviewers allocate more resources and deal certainty commands a premium. That supports the base case for an on-schedule close.

The bear case is simpler: Brent below $85 by end of Q2 removes the energy crisis thesis entirely. At that point, TMTG is a media stub with $3.6 million in quarterly revenue and fusion optionality that requires a decade-long time horizon most retail holders will not sustain. Watch the S-4 date first, Brent through April second, and TAE’s next plasma milestone update third — in that order.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Nothing here should be taken as a recommendation to buy or sell any security or asset. Always do your own research and consult a qualified financial adviser before making investment decisions.