China’s AI lab Manus built a product Meta valued at roughly $2 billion, then Beijing blocked the sale and barred the founders from leaving the country. That’s not a trade dispute. That’s a government telling you exactly which assets it considers strategic — and it’s the clearest single signal of what the Communist Party’s new 15th Five-Year Plan (2026–2030) actually means in practice. The Financial Times reported Beijing is scrutinising the deal over fears of strategic technology flowing overseas. Most coverage frames it as a geopolitical story. Traders should read it as an investment thesis.

What the Masterplan Actually Says

The Economist described the Communist Party’s technological ambition as “breathtaking.” That word choice is doing a lot of work. The 15th Five-Year Plan designates seven strategic emerging industries — AI, semiconductors, EVs and batteries, advanced robotics, quantum computing, biotech, and space — as national priorities, each with specific output targets and market-share objectives that function as performance contracts for state-directed capital. Unlike Made in China 2025, which was aspirational enough to invite Western mockery, this plan is operationalised: the state isn’t just announcing goals, it’s deploying capital at the sector level.

China’s R&D spending as a share of GDP is targeted to reach 3.5% by 2030, up from roughly 2.6% in 2025. That puts China at South Korea’s level — and above Germany. The coverage of this plan in Western financial media has focused almost entirely on the geopolitical friction it creates. That’s the wrong lens. The actionable question is: which sectors have specific, time-bound targets, and who profits or bleeds when China hits them?

The Manus Signal: AI Execution Is Already Ahead of Schedule

The Manus episode is not an isolated data point. DeepSeek R1, released in January 2026, demonstrated that Chinese frontier AI is within striking distance of US models at a fraction of the training cost — approximately $6 million versus $100 million-plus for comparable US systems. Both DeepSeek and Manus were built largely without access to Nvidia H100s at scale, under export controls that were supposed to maintain a permanent US technological lead. The lead is not permanent. The gap is closing faster than the consensus assumed two years ago.

The pattern is consistent: China develops the capability domestically, refuses to let it leave the country, then positions it as a technology export to the Global South. This is the masterplan’s AI chapter playing out in real time, 18 months before the plan’s targets were supposed to pressure-test markets.

Five Sectors Traders Should Focus On

The plan covers seven sectors. Quantum computing, biotech, and space are in it — but their commercialisation horizons are long and liquid instruments are scarce. The five sectors below have near-term revenue implications and tradeable proxies today.

Semiconductors. SMIC has reached 7nm production. CXMT is targeting DRAM cost parity with SK Hynix by 2028. Neither is at leading-edge volume yet — but the trajectory is set. Western export controls slowed the timeline; they didn’t change the destination.

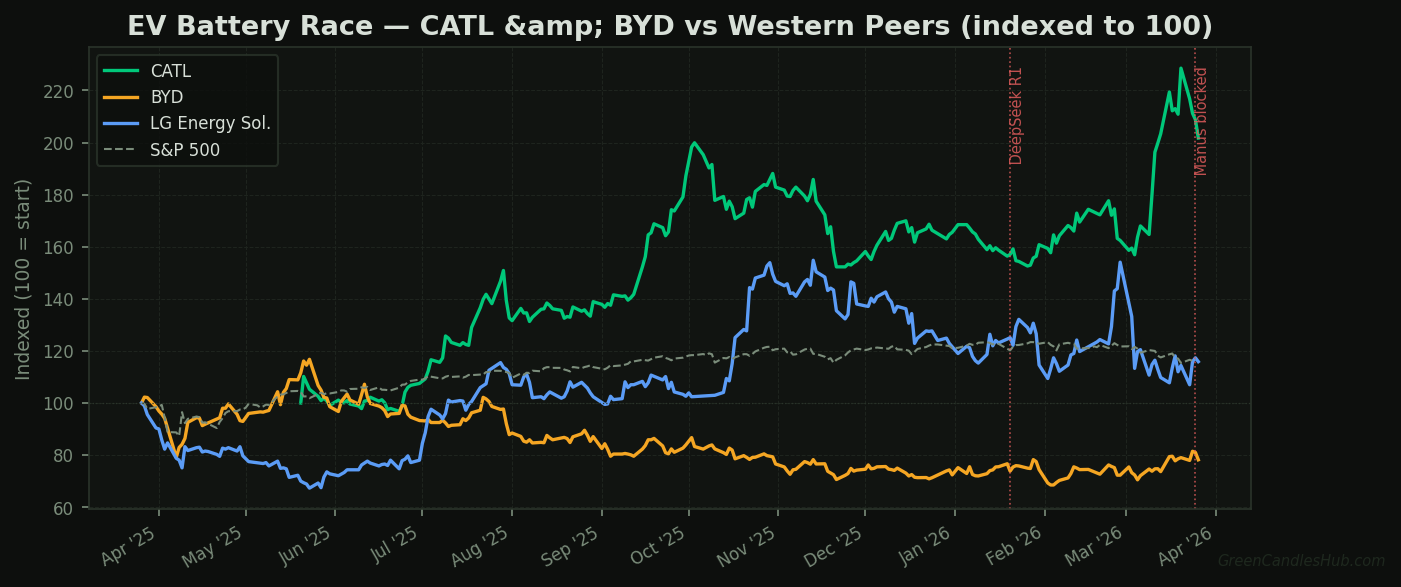

EVs and batteries. China held approximately 65% of global EV sales in 2025. CATL’s share of the global battery cell market exceeds 37%. The Western battery buildout — Northvolt filed for administration in 2025, Panasonic is losing ground — has not produced a competitor that matches CATL’s cost structure. BYD now sells passenger EVs in Europe, South America, and Southeast Asia at price points no Western OEM can match without losing money.

Robotics. Unitree’s H1 humanoid robot ships at under $20,000 per unit. Unitree is not a moonshot startup — it has shipped hardware to customers including research institutions in the United States. Boston Dynamics is still the name most people mention when they discuss humanoid robotics. Unitree is the one shipping at a price point that actually reaches industrial buyers.

AI. Manus, Kimi, and DeepSeek are three frontier-tier systems built without H100 access at scale. Each is already deployed commercially or in controlled testing. The masterplan’s AI targets assume continued domestic development — not US technology access. Export controls are now priced into China’s planning assumptions.

Advanced manufacturing. China’s construction machinery exports surged 33% in the first two months of 2026. Caterpillar and Komatsu are losing emerging-market share to XCMG and SANY, which undercut their pricing by 30–40%. The Business Times noted that AI-related demand is actively shielding Chinese export volumes from the Iran war shock — the sectors the masterplan prioritises are the sectors absorbing the global headwinds.

Which Western Companies Are Most Exposed

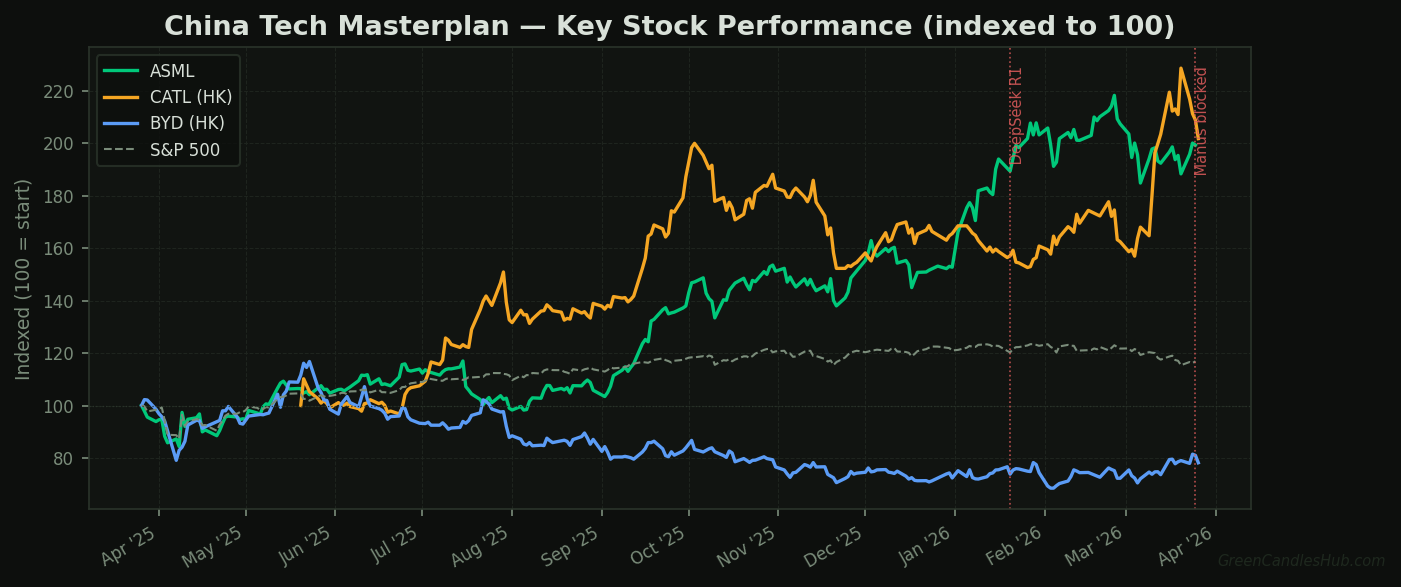

ASML is the one Western company that profits regardless of who wins the semiconductor race. China remains approximately 29% of ASML’s 2025 revenue as Chinese fabs rush to stockpile DUV lithography machines ahead of potential further export restrictions. ASML cannot sell its most advanced EUV tools to China — but the DUV machines it can sell are being bought in volume, and China’s domestic logic-chip buildout guarantees that demand continues.

China already dominates rare earth processing, the upstream chokepoint for both EVs and defence electronics. Western battery cell suppliers cannot match CATL’s scale economics. In robotics and construction equipment, Chinese manufacturers have crossed the quality threshold that previously let Western brands justify their premium. The masterplan’s targets don’t require China to close the last few percentage points of quality gap — they require volume, and volume is already there.

The Tradeable Theses

Long ASML. China’s semiconductor ambition guarantees DUV demand regardless of export control tightening. ASML’s China order book in Q2 2026 earnings (April) is the first clean data point on whether the stockpiling cycle is accelerating or plateauing. The stock trades at a premium to European industrials, and the premium is justified by the structural position.

Long CATL (3750.HK) and BYD (1211.HK) via Hong Kong-listed shares. The masterplan’s EV targets create a direct revenue tailwind for both. BYD’s international expansion and CATL’s contract wins with BMW and Stellantis are already happening; the masterplan accelerates the state support behind them.

Underweight Western EV battery suppliers. Northvolt is already gone. Panasonic’s battery division is losing ground on every margin metric. The cost gap between CATL and the next-closest Western cell manufacturer is not closing. A position that was defensible in 2022 based on IP and scale advantages no longer holds.

Watch Manus AI’s domestic outcome as a leading indicator. If Beijing relists Manus domestically at a higher valuation, it confirms the state will subsidise strategic AI champions rather than let them be acquired or listed abroad. That is a direct read-across to Baidu’s AI cloud division and Alibaba Cloud valuations, both of which are currently priced without full credit for state backing.

What Traders Should Watch

The metric that matters most over the next 24 months is SMIC’s domestic semiconductor yield rate at 7nm. When SMIC hits consistent high-volume production at that node, the Western export control strategy will have been neutralised at its core objective. Goldman Sachs and HSBC both model 2028 as the earliest plausible SMIC high-volume 7nm crossover. The Manus episode suggests the execution timeline is ahead of consensus on AI; the same may be true for chips.

Three signals are worth tracking in the near term: ASML’s China order volume in April Q2 earnings; the Manus AI domestic relisting (if and when it comes); and CATL’s Western OEM contract wins in H1 2026. If all three move in the direction the masterplan implies, the repricing of China tech exposure in Western portfolios — currently heavily underweight — will not be gradual.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Nothing here should be taken as a recommendation to buy or sell any security or asset. Always do your own research and consult a qualified financial adviser before making investment decisions.